The UK Property Market: More Than a Single Story

Welcome to Garrington’s June UK property market review, where another month of competing data and conflicting headlines is...

Welcome to Garrington’s monthly market review, where we explore the trends and influences shaping the UK property market.

After weeks of relentless rain, the arrival of meteorological spring has brought blue sky in more ways than one. Much of the flurry of buyer enquiries and valuation requests that characterised the start of the year is now converting into committed action, with new stock entering the market and purchasers pushing forward with their house hunting in earnest.

The pricing picture across the major indices points to stability rather than momentum. Both Halifax and Nationwide’s price indices recorded average house values rising by 0.3% in February. Annual growth stands at 1% according to Nationwide, while Halifax put annual growth at 1.3% and the average price at a new high of £301,151. Rightmove’s data adds useful further perspective. After a record January jump, February asking prices held flat, yet the combined rise of 2.8% since December still represents the strongest start to a year since 2020, driven by pent-up confidence after the prolonged Budget uncertainty of late 2025.

Rightmove’s data adds useful further perspective. After a record January jump, February asking prices held flat, yet the combined rise of 2.8% since December still represents the strongest start to a year since 2020, driven by pent-up confidence after the prolonged Budget uncertainty of late 2025.

Garrington is seeing sellers recalibrate as the realities of a more competitive landscape set in. With the number of homes for sale at an eleven-year high, buyers have genuine choice and greater leverage, resulting in deals being agreed at levels that would have been simply dismissed six months ago.

Off-market activity is also rising, which is partly seasonal with stock quietly offered ahead of Easter, but notwithstanding this, Garrington is seeing meaningful volumes of property changing hands privately, creating purchasing opportunities for well-connected buyers that remain invisible to the wider market. While the national picture is encouraging, the detail reveals a UK property market moving at very different speeds.

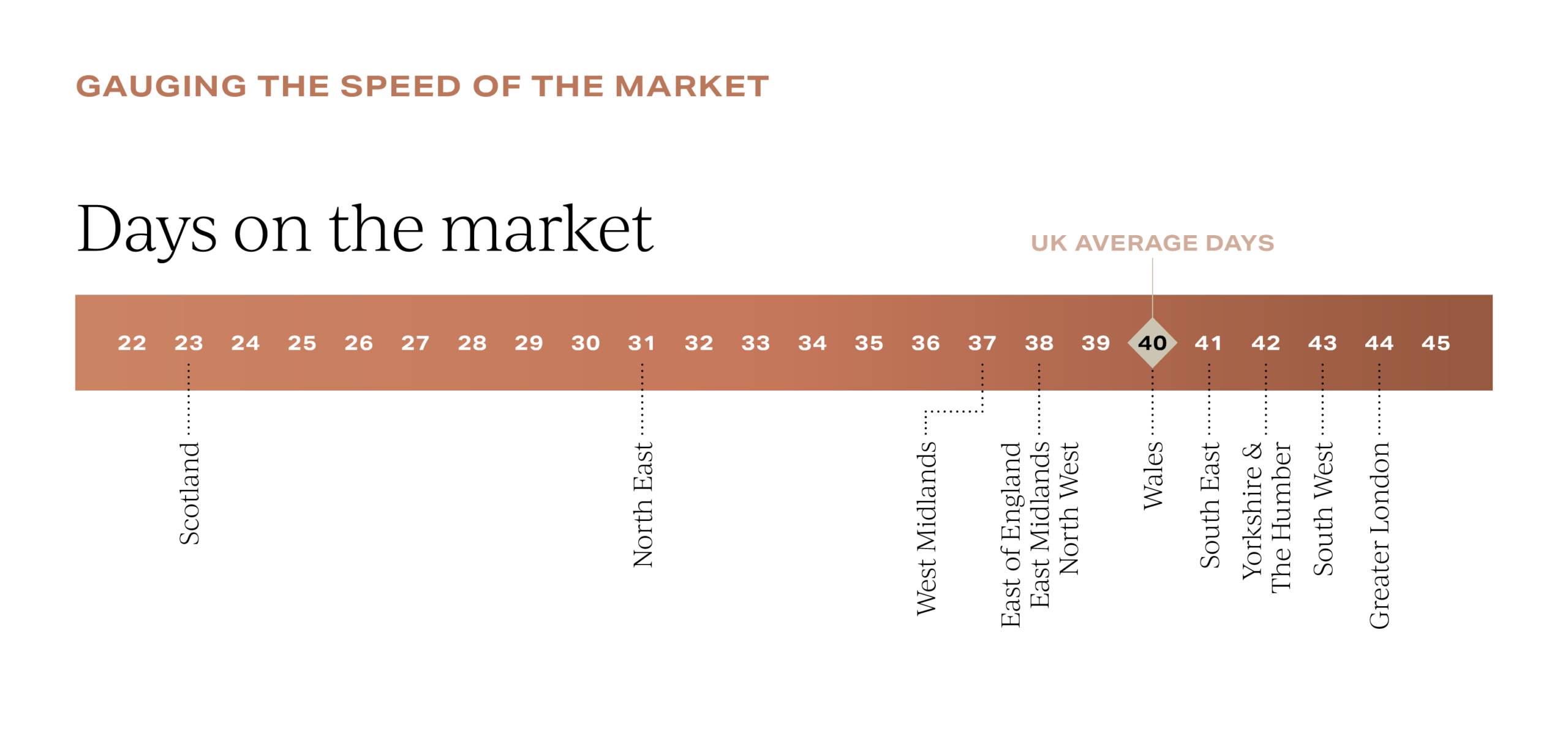

New data shows the average time to sell in England and Wales stands at 40 days, but Greater London averages 44 and the South East 41, reflecting persistent price sensitivity in higher value southern markets. Scotland is the fastest at just 23 days, followed by the North East at 31.

These figures underline a point that Garrington has been making for some time; pricing accuracy from the outset is the single most important factor in achieving a timely sale.

Beneath regional variations, the domestic fundamentals are moving in an encouraging direction. Hometrack reports that sales agreed ran at one of the strongest February levels of the past decade, with mortgage rates at a four-year low and new listings on track to hit a decade high. Available stock is already 6% above year-ago levels, giving buyers more choice while keeping price growth contained.

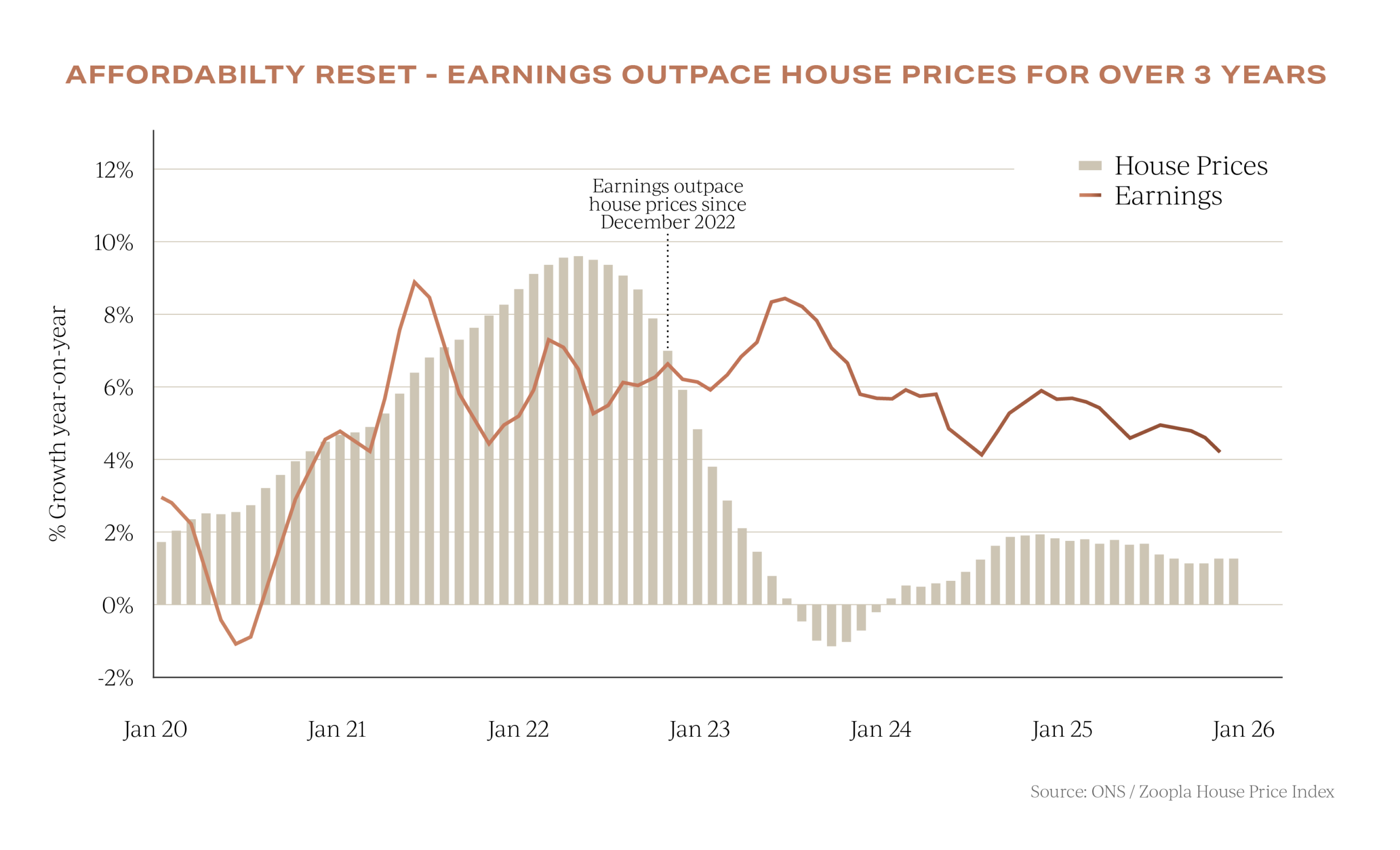

The affordability picture has shifted more than many expected.

Hometrack estimates that 40% of homes for sale can now be bought for less per month with a mortgage than renting locally, up from 25% a year ago. Nationwide’s research shows repayments for a typical first-time buyer represent around 32% of take-home pay, close to the long run average of 30%, and the house price-to-earnings ratio has improved to 4.7, just below its 20-year average.

With average earnings growth having outpaced average house price inflation for three consecutive years, the fundamentals underpinning buyer demand are stronger than at any point since 2022.

The wider international backdrop, however, introduces a note of caution. Ongoing geopolitical tensions and the conflict in the Middle East have the potential to influence energy prices and inflation expectations, which in turn shape the outlook for central bank interest rates. Even small shifts in these expectations can affect mortgage pricing, and some lenders have already adjusted their most competitive fixed-rate products in recent weeks.

It remains too soon to judge the full impact, but the trajectory of borrowing costs will play an important role in determining how quickly the housing market recovery gathers pace.

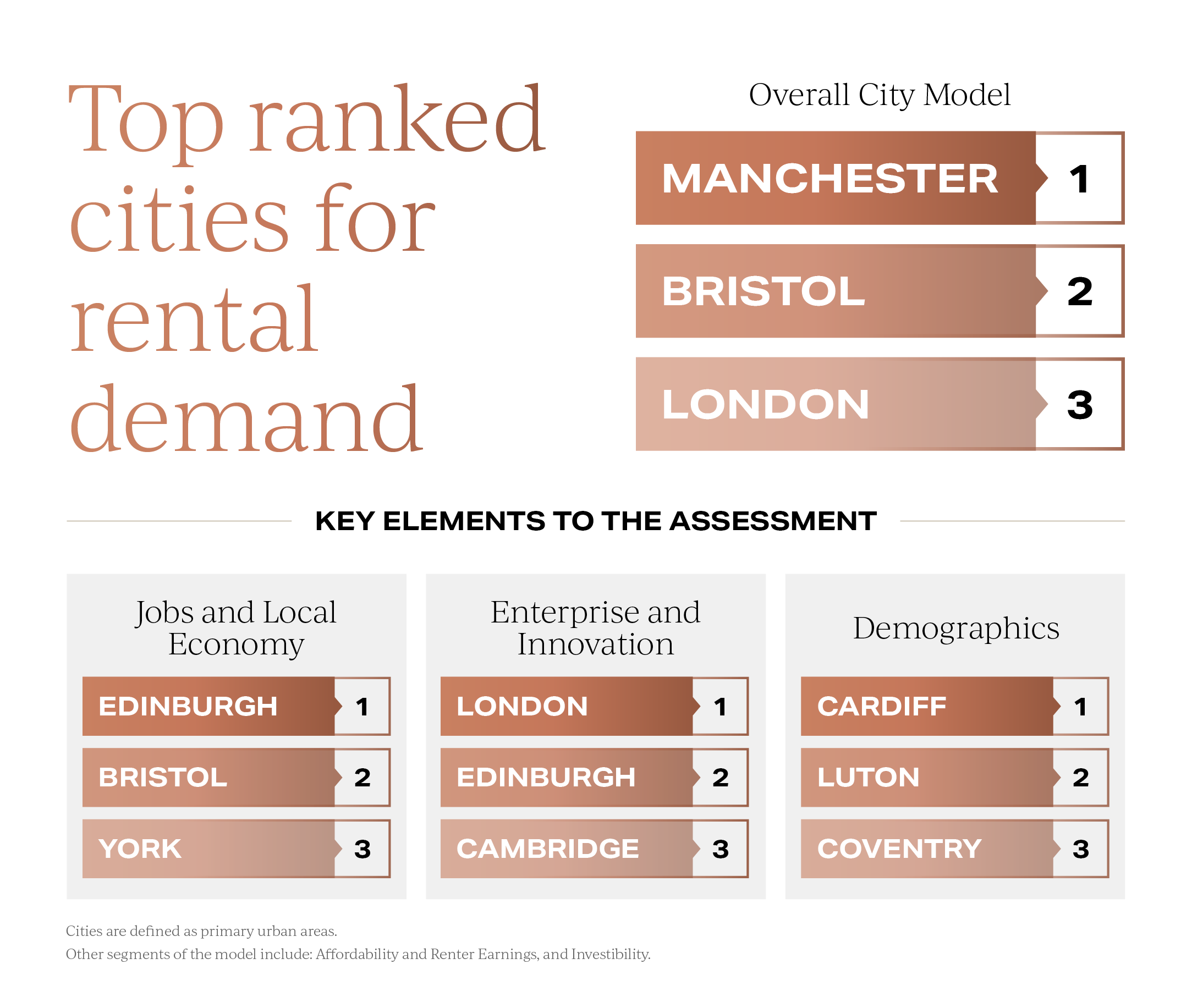

Despite improved levels of affordability, tenant demand is gathering pace in many parts of the UK.

New research identifies Manchester, Bristol and London as the strongest rental markets in the UK, with Edinburgh, York and Bristol once again leading on job creation and knowledge economy concentration. The emergence of Aldershot, Newcastle and Norwich as new top ten entrants signals that rental demand drivers are spreading well beyond traditional urban centres.

London remains uniquely complex, with its global employment base attracting strong tenant demand while the cost of ownership keeps many would-be buyers renting. For international purchasers and relocating professionals, renting provides a practical first step before committing to a purchase.

Reflecting this sustained demand, Garrington has recently expanded its London rental search service. To find out more, please do get in touch.

The prime sector tells a markedly different story. Garrington is seeing encouraging activity between £750,000 and £2 million, where committed buyers are returning with growing confidence. Above that level, the UK property market is more selective, though at £5 million and above, there are reassuring signs of fresh opportunity ahead of the traditionally busier spring season.

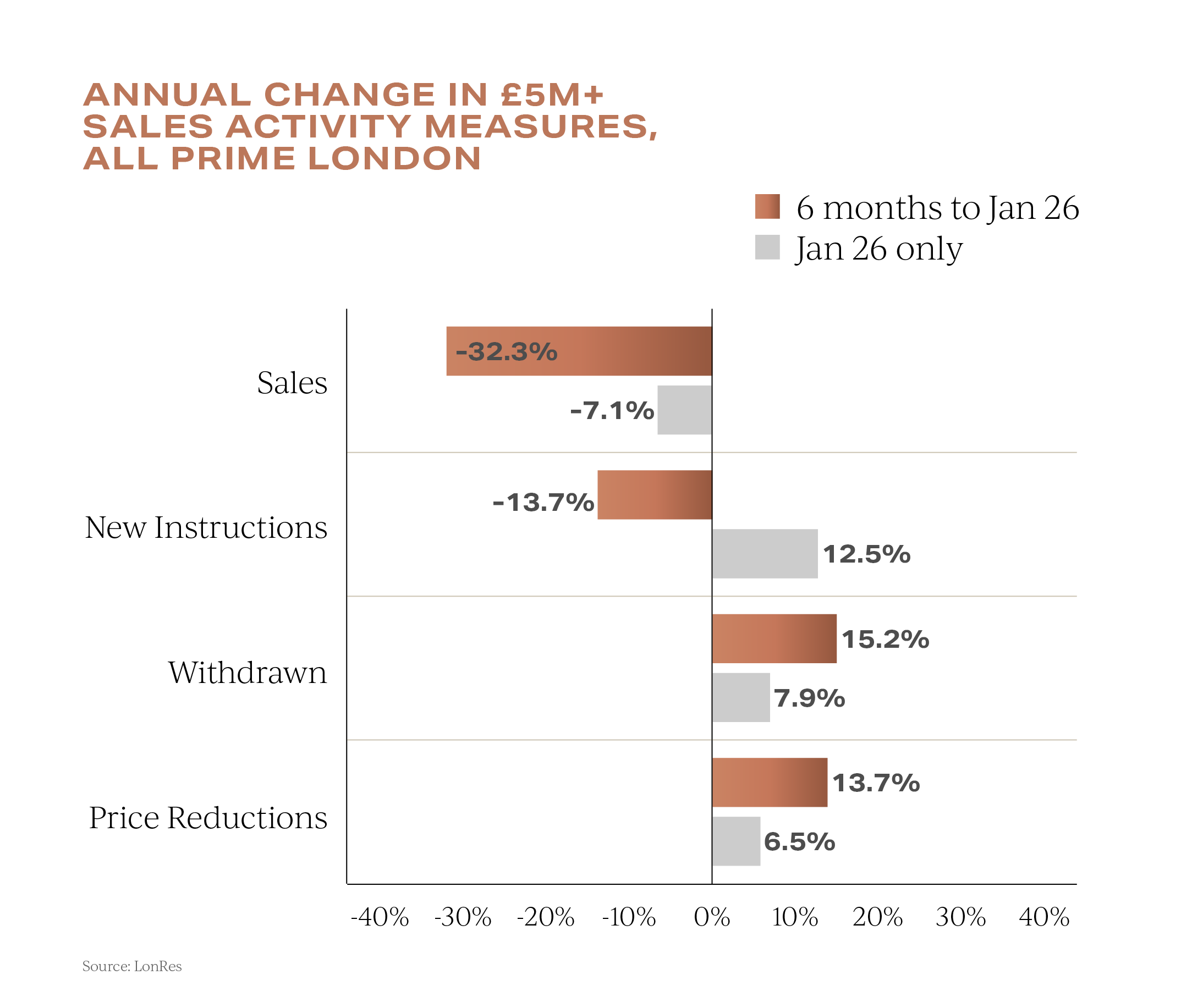

LonRes data quantifies the adjustment in prime London, where transactions fell just over 30% year-on-year in January, achieved prices declined 5.6%, and the average discount from asking price sits at 10.3%.

More than half of properties sold had undergone at least one price reduction, the highest proportion since late 2018.

At the super-prime level, new instructions above £5 million hit a record January figure, up 12.5% year-on-year, while transactions fell 7.1% and available stock grew by nearly 10%. Rightmove’s top of the market segment mirrors this nationally, with asking prices down 0.2%, despite the second-stepper feeder market posting modest gains.

Last month’s RICS twelve-month outlook returned its most positive reading since February 2025, with 43% of respondents expecting prices to be higher in a year. This remains, however, a recovering rather than a rising market, and the months ahead will be shaped as much by global events as by domestic sentiment.

For those at the early stages of planning a move this spring, Garrington’s Best Places to Live in 2026 research provides a valuable resource. The interactive tool allows users to compare locations across the UK based on a range of lifestyle and investment factors, helping buyers shape their thinking and refine their search.

For well-advised buyers, the combination of improved affordability, abundant choice and growing seller realism could create a favourable spring market. If Garrington can help with your property plans, do get in touch.

Welcome to Garrington’s June UK property market review, where another month of competing data and conflicting headlines is...

Welcome to Garrington’s latest UK property market review. May is the first month this year in which both the...

Welcome to Garrington’s latest UK Property Market Review. The clocks have sprung forward, the evenings are lengthening, and...