The UK Property Market: More Than a Single Story

Welcome to Garrington’s June UK property market review, where another month of competing data and conflicting headlines is...

Welcome to Garrington’s latest UK property market review.

May is the first month this year in which both the data and our own observations reflect how the market is performing under the conditions that have emerged in recent weeks.

In April, financial markets had already reacted while housing data had yet to catch up; May, however, provides a more nuanced answer than either reading alone would have suggested.

On the ground, the market is still functioning, but with a clearer line between the homes that are selling and those that are not. Best-in-class properties continue to sell quickly and close to the prices vendors expect, while anything compromised by location, condition or pricing meets greater resistance.

Vendors holding out for yesterday’s valuations are being passed over, and correct pricing is now what brings serious buyers to the table.

The headline figures bear that out, with the major indices reading the market in slightly different ways. Nationwide reported annual UK house price growth lifting to 3.0% in April, from 2.2% in March. Halifax, by contrast, recorded prices easing 0.1% over the month and annual growth slowing to 0.4%. Rightmove’s new seller asking prices rose 0.8% against supply at an eleven-year high for the time of year, while Hometrack records sales agreed 3% below last year, and the average home selling in 33 days, one more than a year ago.

Rightmove’s new seller asking prices rose 0.8% against supply at an eleven-year high for the time of year, while Hometrack records sales agreed 3% below last year, and the average home selling in 33 days, one more than a year ago.

Beneath those headlines, the market’s structural supports remain in place. Household debt sits at its lowest level relative to income for around two decades, and wage growth of 3.9% has continued to outpace house price growth across the major indices, supporting affordability over time.

Nationwide and several other major high-street lenders have widened their loan-to-income criteria for qualifying borrowers, with some now offering up to six times income. For those committed to moving, the means to act has broadened rather than narrowed.

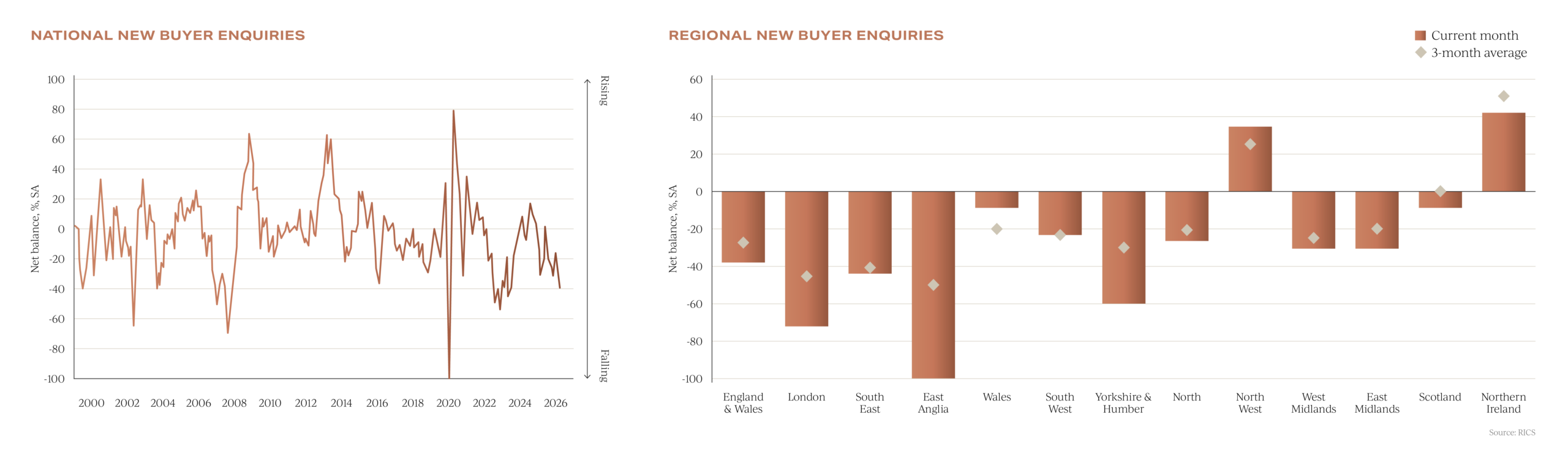

The forward-looking indicators read in the other direction. The April-released RICS Residential Market Survey recorded new buyer enquiries at a net balance of minus 39%, the weakest since August 2023, with near-term sales expectations slipping from minus 4% to minus 33%.

The Bank of England held the Bank Base Rate at 3.75% on 29 April by eight to one, with the one dissenting vote favouring an increase rather than a cut.

Alongside these readings, we are seeing the re-emergence of needs-based buyers: those requiring more space, downsizers, movers for work or schools, and households with mortgage offers approaching expiry. They are cautious but not inactive, well-prepared and decisive when the right home appears.

Hometrack records enquiries rebounding after Easter to their highest level since the conflict began, with lenders competing for business once more. The UK property market is functioning, stronger today than the months ahead suggest.

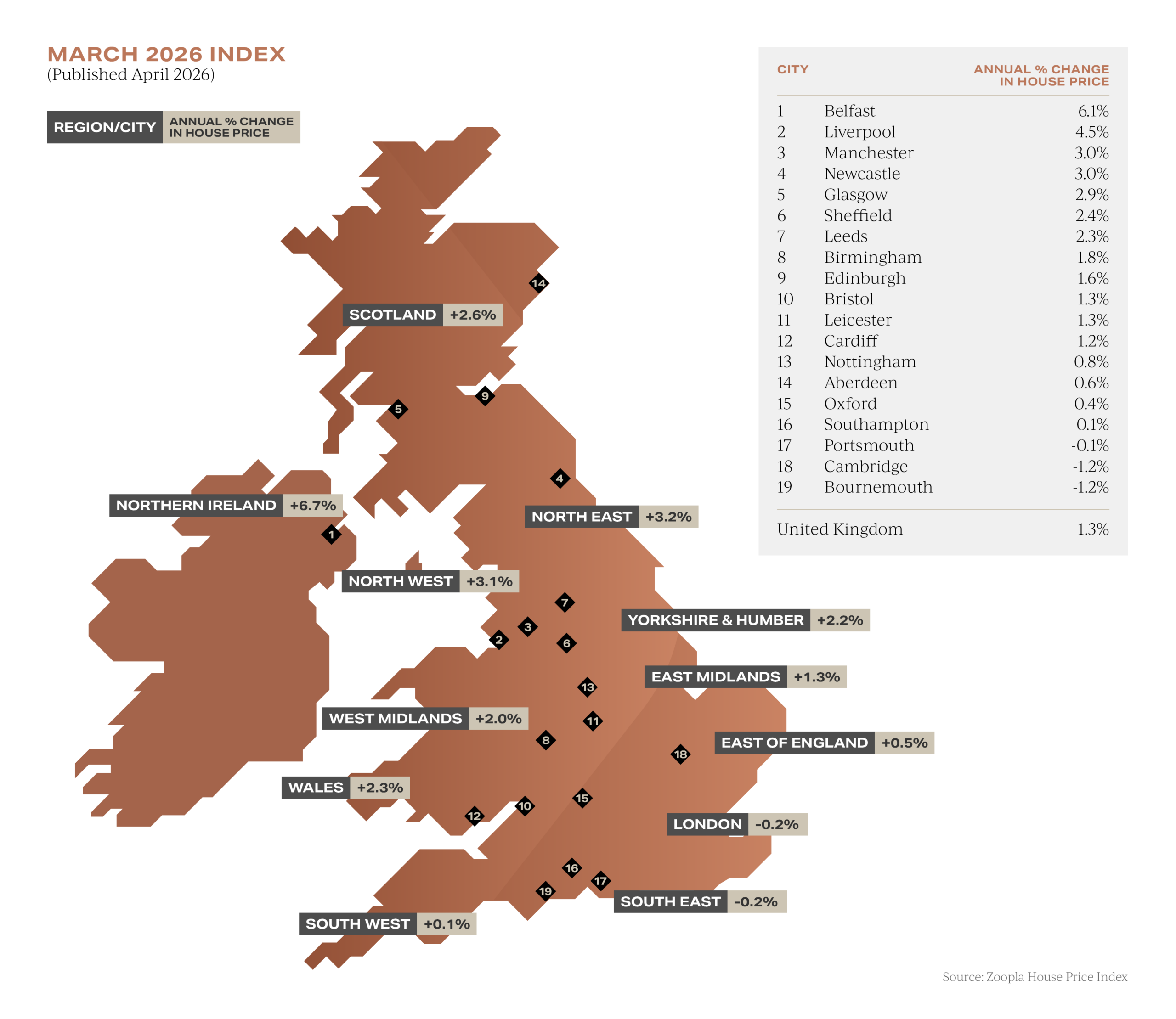

National averages are concealing as much as they reveal, and the gap between regions is widening. The latest ONS UK House Price Index shows annual growth ranging from 3.9% in Yorkshire and the Humber to minus 3.3% in London, with Northern Ireland at 7.5% in the year to the fourth quarter of 2025.

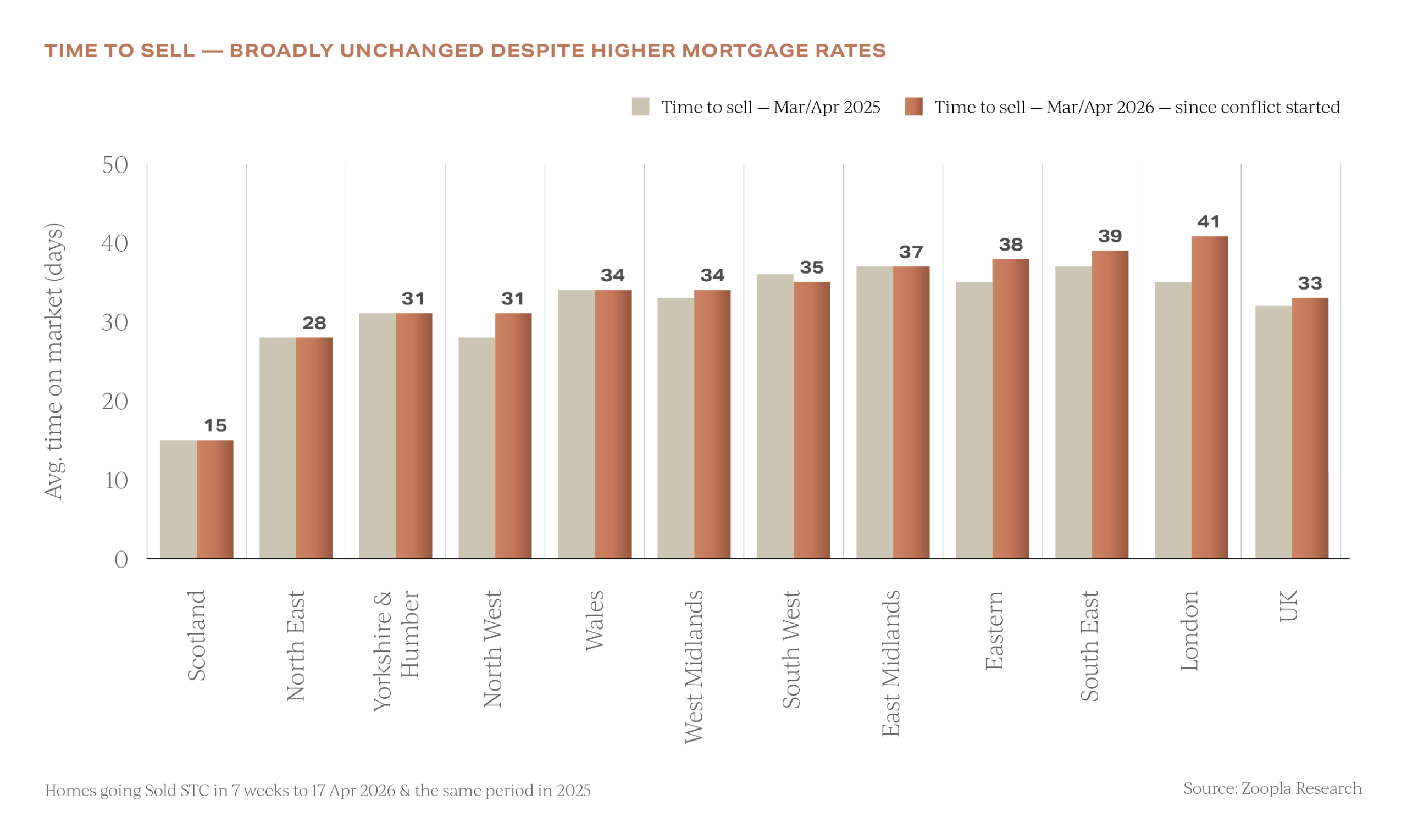

Hometrack reinforces the pattern: every city in its index with annual growth above 3% sits in the North of England, while every city recording annual price falls sits in southern England. The same dispersion is visible in time on market. Hometrack data also shows that across more than half of UK regions, time to sell is unchanged or shorter than a year ago, while increases are concentrated in outer London and the commuter belt, where first-time buyer mortgage and stamp duty sensitivity is greatest.

The same dispersion is visible in time on market. Hometrack data also shows that across more than half of UK regions, time to sell is unchanged or shorter than a year ago, while increases are concentrated in outer London and the commuter belt, where first-time buyer mortgage and stamp duty sensitivity is greatest.

In some of those markets, time to sell a property has risen by 30 to 65% year on year, but increasingly the local picture is telling more of the story than the national figures alone.

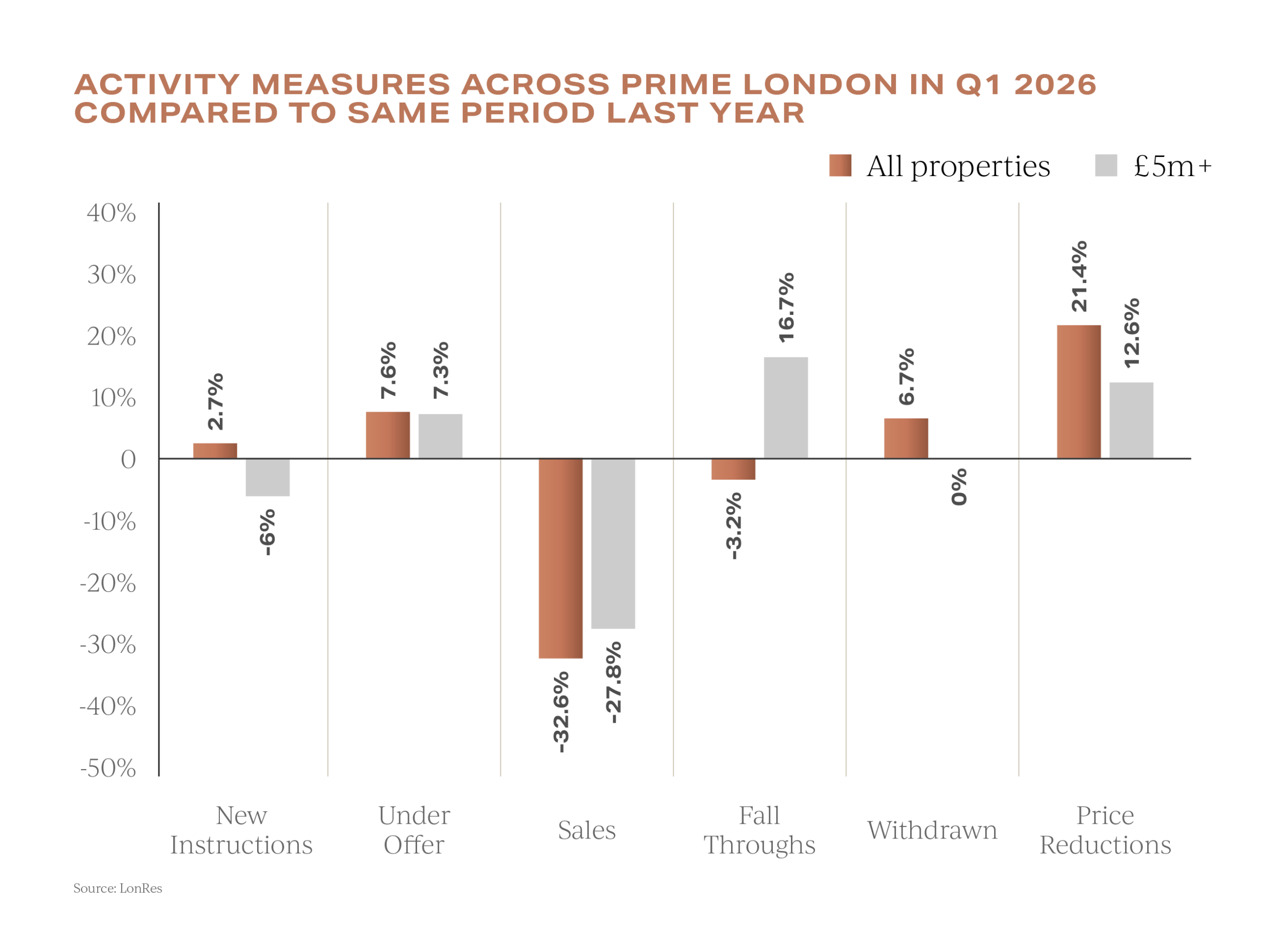

Prime London is a market apart, and within it the picture is far from uniform. LonRes reports first-quarter sales volumes across prime London fell 32.6% year on year, prime central London achieved prices 7.0% lower, and average discounts from asking to sale ran at 14.2% in prime central London, well above long-term levels.

First-quarter under-offer numbers were nonetheless 7.6% higher year on year and 35% above the pre-pandemic average, suggesting forward activity that headline volumes have yet to capture. April also produced what is said to be the largest UK residential sale on record, with Providence House reportedly changing hands for £275 million.

April also produced what is said to be the largest UK residential sale on record, with Providence House reportedly changing hands for £275 million.

The divide at the top of the UK property market has rarely been more pronounced: buyers acting on long-term conviction continue to transact, while the broader prime market remains highly price sensitive.

May also brings the most significant change to the residential lettings sector in a generation, with the Renters’ Rights Act which came into force on the 1st of May. Fixed-term tenancies no longer apply, Section 21 no-fault notices are abolished, and rent increases must follow a defined annual process.

TwentyCi reports the proportion of for-sale listings that are former rentals has fallen from 22.5% in the first quarter of 2025 to 12.4% in the first quarter of 2026, while industry data places the total value of private rented sector stock today, at around £79 billion below its 2022 level.

Much of the landlord adjustment feared has therefore already taken place. How tenants, landlords and investors respond now that the new framework is live is the next question to answer.

Put simply: there are fewer discretionary buyers, vendors on and off-market are more willing to talk, and the conditions for a well-prepared move are quietly improving. For now, the uncertain consequences of events in the Middle East sit at the edge of buyers’ thinking rather than at the centre of it.

In May, preparation matters more than speed, and as the process moves on, clarity on property, price and position is what counts. For buyers who know what they want and can move when the moment comes, this could prove one of the more interesting buying windows of the year.

To discuss how these conditions apply to your own circumstances, please get in touch. We look forward to sharing our latest insights next month.

Welcome to Garrington’s June UK property market review, where another month of competing data and conflicting headlines is...

Welcome to Garrington’s latest UK Property Market Review. The clocks have sprung forward, the evenings are lengthening, and...

Welcome to Garrington’s monthly market review, where we explore the trends and influences shaping the UK property market. After...