The Spring UK Property Market: Recovering, not Rising

Welcome to Garrington’s monthly market review, where we explore the trends and influences shaping the UK property market. After...

Welcome to Garrington’s latest UK Property Market Review. The clocks have sprung forward, the evenings are lengthening, and for thousands of prospective buyers, the Easter break has provided a welcome moment to sit down with family, take stock, and begin shaping plans for the months ahead.

Longer days mean more time for viewings, and gardens and outdoor spaces can finally be properly assessed. The traditional surge in new listings is giving buyers more homes to look at than at any point in the past eleven years.

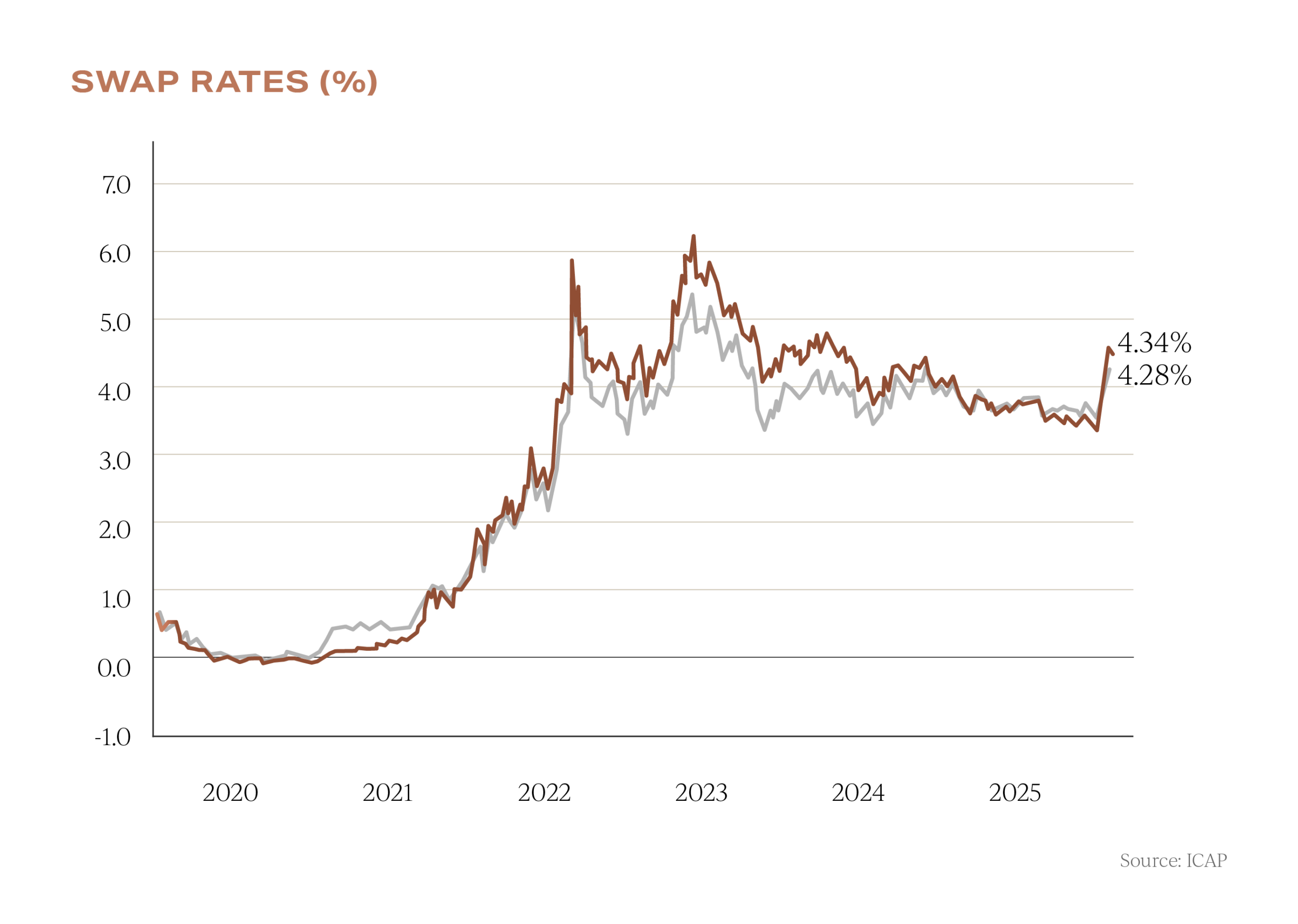

This spring, however, the biggest forces shaping sentiment are not appearing first in estate agents’ windows. They are emerging from bond yields, swap rates, and mortgage pricing desks. The property market and the financial markets appear to be operating at very different speeds, and understanding the gap between the two may be the most important factor in making a well-timed property decision this year.

In the financial markets, the response to recent global events has been swift. Swap rates have risen sharply, expectations of Bank of England rate cuts have tempered, and by late March three interest rate increases were priced in over the next twelve months; a dramatic reversal from the two cuts anticipated just weeks earlier. Rightmove’s daily tracker shows the average two-year fixed rate jumping from 4.24% to 4.51% in a single week, with many sub-4% deals being withdrawn altogether.

Rightmove’s daily tracker shows the average two-year fixed rate jumping from 4.24% to 4.51% in a single week, with many sub-4% deals being withdrawn altogether.

Despite this, housing data has, so far, remained broadly stable. Nationwide reports annual house price growth picking up to 2.2% in March, with the average UK property now valued at £277,186. Zoopla holds annual inflation steady at 1.3%. Rightmove recorded a typical seasonal monthly rise of 0.8%. But business as usual does not mean business without caution.

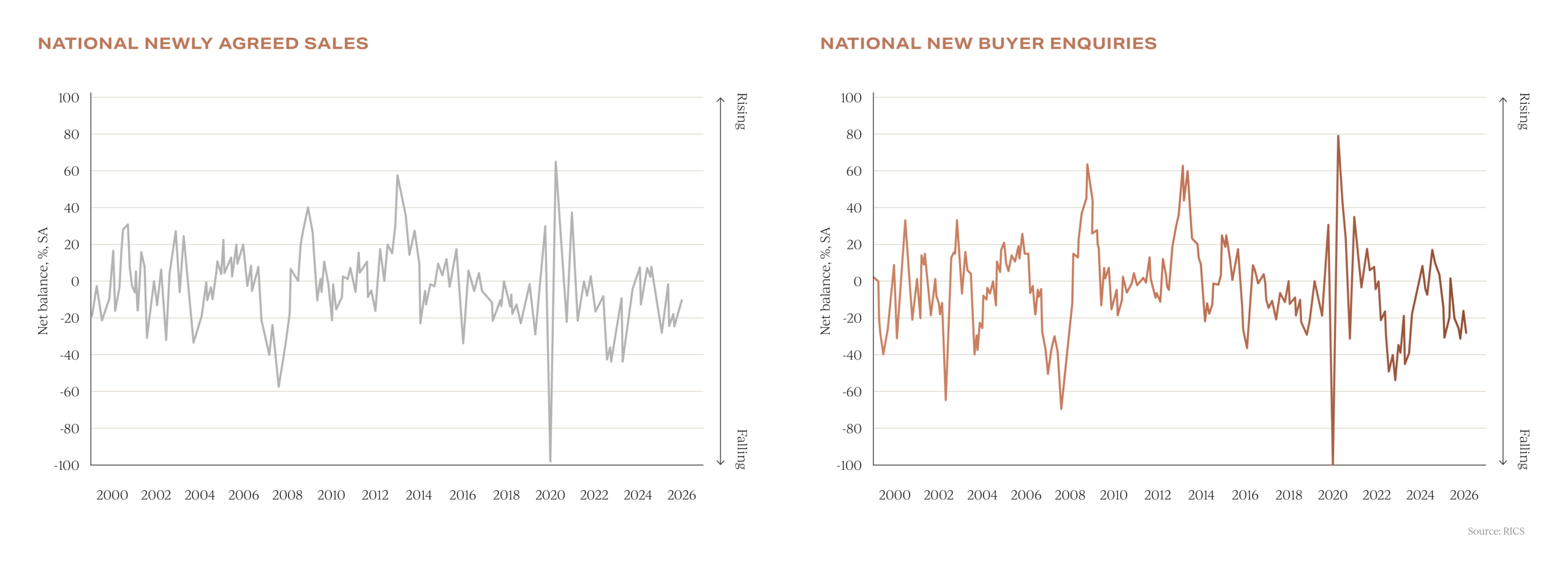

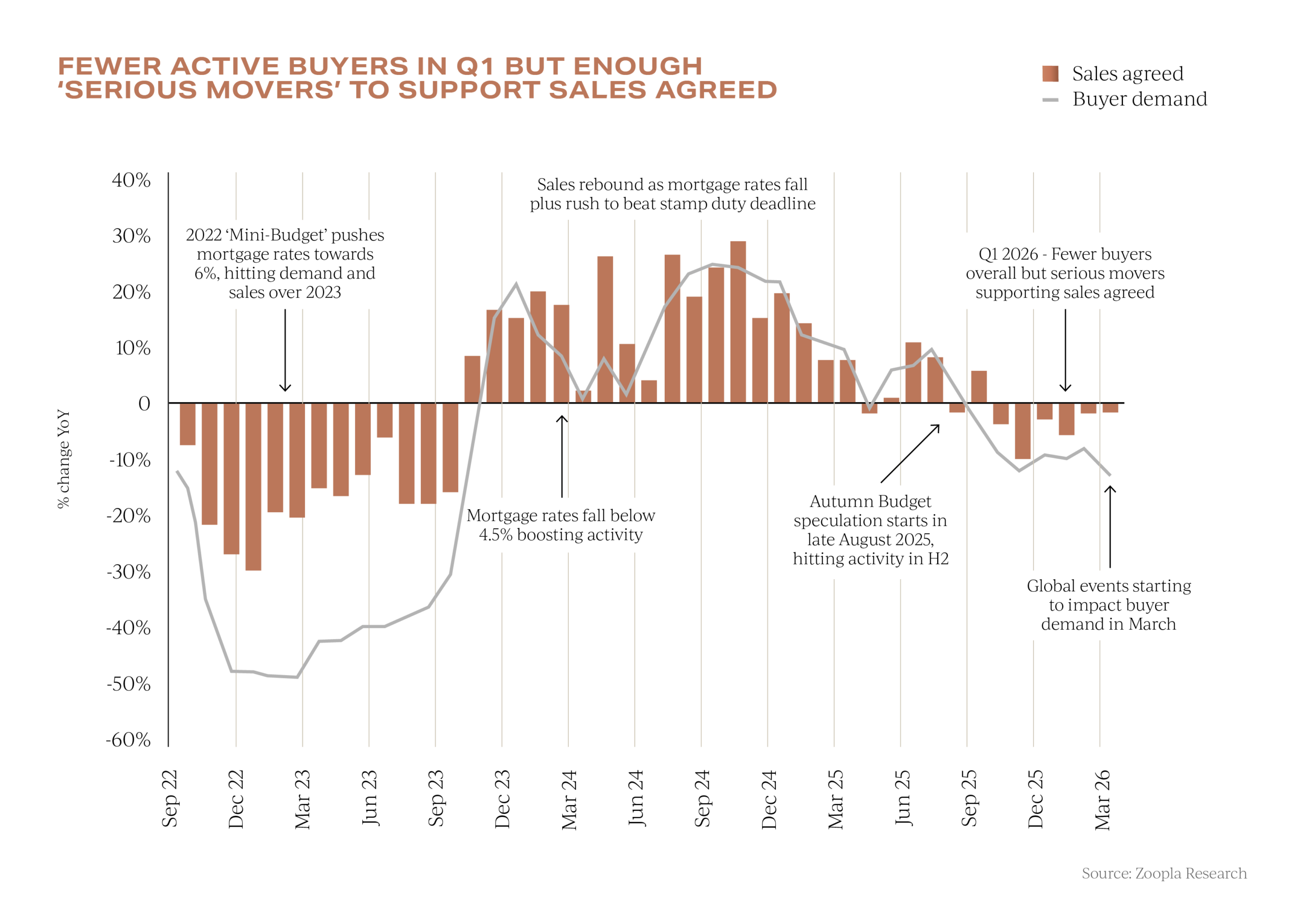

The RICS Residential Market Survey, published last month, shows new buyer enquiries at a net balance of -26% in February, with agreed sales at -12% and near-term expectations softening. Activity is holding up, but confidence is more fragile than headline numbers alone would suggest.

Could uncertainty actually work in a buyer’s favour? Zoopla’s data suggests it can. Buyer enquiries are running 13% below last year, as early-stage and discretionary purchasers adopt a more cautious stance.

Hometrack says sales agreed are only 2% below last year, while according to Rightmove they remain 5% ahead of 2024. That is precisely the combination that can open a buying window: more stock, fewer competing offers, and sellers who understand that affordability still matters.

Those who remain active are serious, financially prepared, and pressing ahead with clear intent. Zoopla reports no difference in commitment between first-time buyers and existing homeowners. Around a quarter of all sales are cash purchases, while many existing homeowners have built up sizeable equity positions. Garrington is seeing the same pattern. Early-stage buyers are taking more time, assessing how conditions develop. But those we are actively advising remain focused and determined to secure the right property at the right price.

Around a quarter of all sales are cash purchases, while many existing homeowners have built up sizeable equity positions. Garrington is seeing the same pattern. Early-stage buyers are taking more time, assessing how conditions develop. But those we are actively advising remain focused and determined to secure the right property at the right price.

With the choice of homes for sale running 6% above last year, committed buyers are finding less competition and genuine room to negotiate.

For buyers holding US dollars, the opportunity extends well beyond softer pricing. Sterling’s recent weakness has created a substantial additional advantage that compounds with every increase in property value.

According to Lumon, a property priced at £500,000 cost $35,500 less in dollar terms at the end of March than in late January. At £1 million the saving reaches $71,000. At £1.5 million it rises to $106,500, and at £3 million the currency-driven reduction stands at $213,000. When these figures are set alongside increased supply and reduced competition, the conditions for well-advised international buyers are, in Garrington’s view, among the most favourable they have been in several years.

When these figures are set alongside increased supply and reduced competition, the conditions for well-advised international buyers are, in Garrington’s view, among the most favourable they have been in several years.

This is particularly relevant in London. The broader capital is showing tentative improvement, with Nationwide’s quarterly data recording annual growth of 1.7%, the strongest of any southern English region.

But at the prime end, LonRes reports that transaction volumes in February fell 31.2% year-on-year, achieved prices declined 10.0%, and in the £5 million-plus market transactions fell 54.8%. London has not yet turned the corner. What is shifting, however, is forward-looking activity. Under offers rose 8.1% annually and new sales instructions are running 34.8% above pre-pandemic averages, suggesting that both buyers and sellers are positioning for what comes next. CBRE expects London prices to edge higher by 0.5% in 2026, with supply shortages supporting stronger growth later in their forecast period.

What is shifting, however, is forward-looking activity. Under offers rose 8.1% annually and new sales instructions are running 34.8% above pre-pandemic averages, suggesting that both buyers and sellers are positioning for what comes next. CBRE expects London prices to edge higher by 0.5% in 2026, with supply shortages supporting stronger growth later in their forecast period.

Across the wider UK property market, Garrington is seeing growing urgency among buyers who secured mortgage offers earlier in the year. These buyers are acutely aware that their offers carry an expiry date, and that any replacement product could come at a materially higher cost.

The pressure to agree terms and move to exchange before that window closes is becoming a significant driver of current activity. This price sensitivity is evident everywhere. Rightmove reports the longest average time to find a buyer at this point in the year since 2013.

Sellers who price realistically from the outset are completing sales.

Those testing the market with optimistic figures are being passed over. Accurate pricing from day one is essential.

This spring market is both resilient and vulnerable. Prices are still rising in some parts of the UK, sales are still completing, and committed buyers are finding genuine opportunities. But borrowing costs have moved sharply, the pool of active buyers is narrowing, and the gap between financial market expectations and property market reality cannot widen indefinitely.

For those with the clarity, the readiness, and the professional guidance to act decisively, this is a market offering real value. The challenge is recognising it in time.

At the time of recording, a short-term ceasefire in the Middle East has been announced, prompting an immediate response in financial markets. Whether this proves to be a turning point or a temporary pause remains uncertain, and as ever, any impact on the UK property market is likely to take longer to emerge.

If you are considering your own property plans, Garrington would be delighted to help you interpret the signals, identify the right opening, and move from a position of strength. Please do get in touch to discuss your requirements.

We look forward to sharing our latest insights next month.

Welcome to Garrington’s monthly market review, where we explore the trends and influences shaping the UK property market. After...

The UK property market begins 2026 with renewed energy. Following the protracted uncertainty that clouded late 2025, last...

As the year concludes, the UK property market is gradually regaining its composure after an autumn shaped by speculation,...