The UK Property Market: More Than a Single Story

Welcome to Garrington’s June UK property market review, where another month of competing data and conflicting headlines is...

Welcome to Garrington’s July UK Property Market Review. Summer is now in full swing, bringing Wimbledon, the cricket, a World Cup, and the holidays that give many of us a first real pause to take stock.

The market has caught the season’s mood, with buyers in less of a hurry and sellers guided by realism rather than optimism.

The forces behind that mood are coming, for once, not from the data but from Westminster, where a forthcoming change of Prime Minister, reform of how homes are bought and sold, and a live debate over property taxation, have left movers with more questions than answers. Yet the market is not holding its breath.

Garrington’s experience is that those who need to move are getting on with it, in disciplined fashion, while those who want to move are split between the undeterred and the wait-and-see.

At a headline level the picture is mixed rather than weak. Nationwide reports annual house price growth edging up to 2.2% in June, though prices were broadly flat over the month, while Rightmove’s asking prices show a 0.6% fall, the largest June drop in fourteen years. One measures what buyers actually pay at mortgage approval, the other what sellers first ask, and Garrington’s read is that sellers are doing the adjusting, narrowing the gap from their side. That is how overpricing corrects, not how a downturn begins.

One measures what buyers actually pay at mortgage approval, the other what sellers first ask, and Garrington’s read is that sellers are doing the adjusting, narrowing the gap from their side. That is how overpricing corrects, not how a downturn begins.

With the increasing likelihood of a new Prime Minister this month, speculation has turned to what a change would mean for housing. In our view what matters is less the name than whether new leadership brings fresh confidence and clarity to questions about future tax and housing policy. The Autumn Budget will sharpen those questions, though few movers are delaying for it.

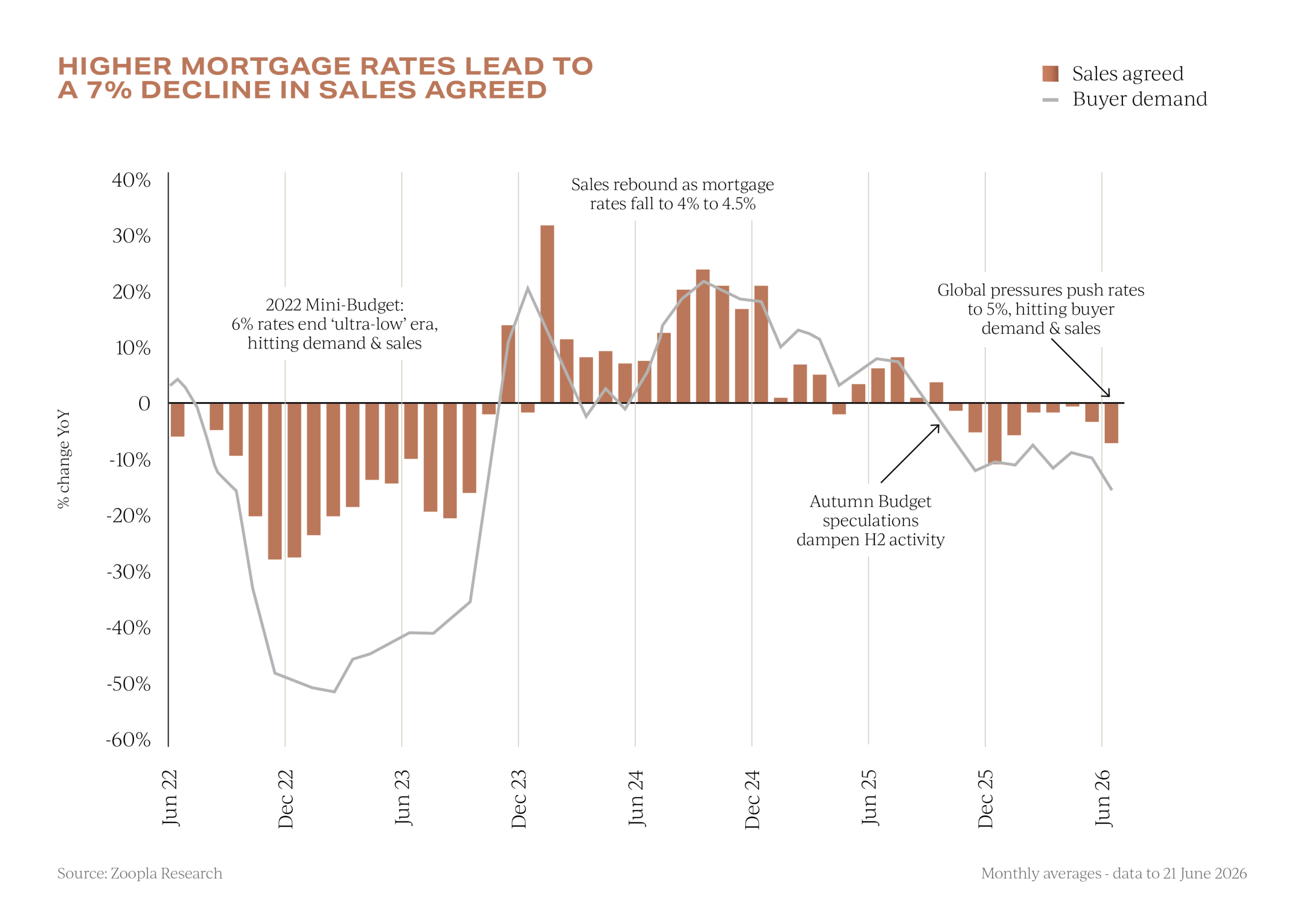

The data bears this out. Zoopla’s latest UK House Price Index picks out political uncertainty, alongside higher mortgage rates, as a drag on activity, with buyer enquiries 15% lower and sales agreed 7% down on the year, while RICS records that demand and sales balances are still firmly negative but, for the first time since January, no longer worsening. The buyers who have stepped back have not gone away; they are waiting for the picture to clear.

The buyers who have stepped back have not gone away; they are waiting for the picture to clear.

Last month’s most significant development had little to do with prices. The government’s newly announced ‘home buying and selling reform roadmap’ sounds procedural, but its implications are wide. By its own figures, a sale takes around 120 days to complete once an offer is accepted, roughly 60% longer than in 2007, and close to one in three transactions still falls through.

The reforms point to upfront sales packs before listing, digital logbooks and, eventually, binding conditional contracts, echoing elements of the Scottish system.

The case for change is plain. RICS puts the average sale at 21.5 weeks from listing to completion, the longest since its records began in 2017, and a drawn-out transaction is a fragile one, more exposed to the renegotiation, fatigue and broken chains the reforms aim to reduce. In Garrington’s view the wide-ranging recommendations are long overdue and likely to be well received by buyers and sellers alike.

The sharpest policy question is at the top of the UK property market. The proposed High Value Council Tax Surcharge, or mansion tax, is under consultation and expected to apply from April 2028 to homes in England valued above £2 million. It appears already to be influencing behaviour, with recent industry research suggesting softer values have pushed more homes below the £2 million line.

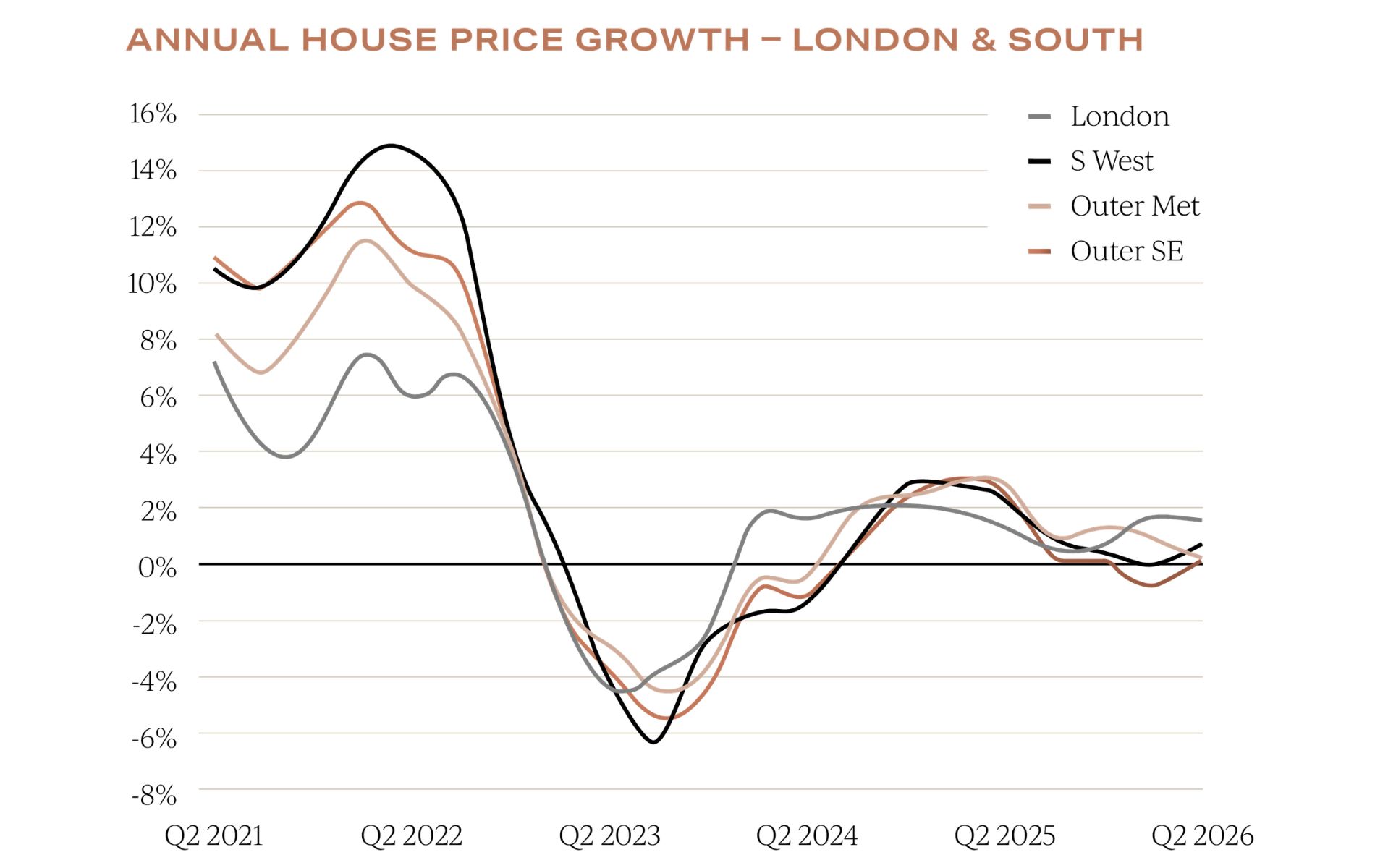

As we discussed last month, London continues to show tentative signs of improvement, with pricing that has adjusted and buyers who increasingly sense value.

The headline indices still tell different stories. Nationwide’s Q2 data has the capital back to 1.6% annual growth, the strongest of the southern regions, with the average home near £541,000, while the official UK House Price Index, which records completed sales months later, puts prices down 2.1% in the year to April, the weakest of any English region.

They are timestamps of different points in the same cycle, describing a selective, postcode-by-postcode stabilisation rather than a broad rebound.

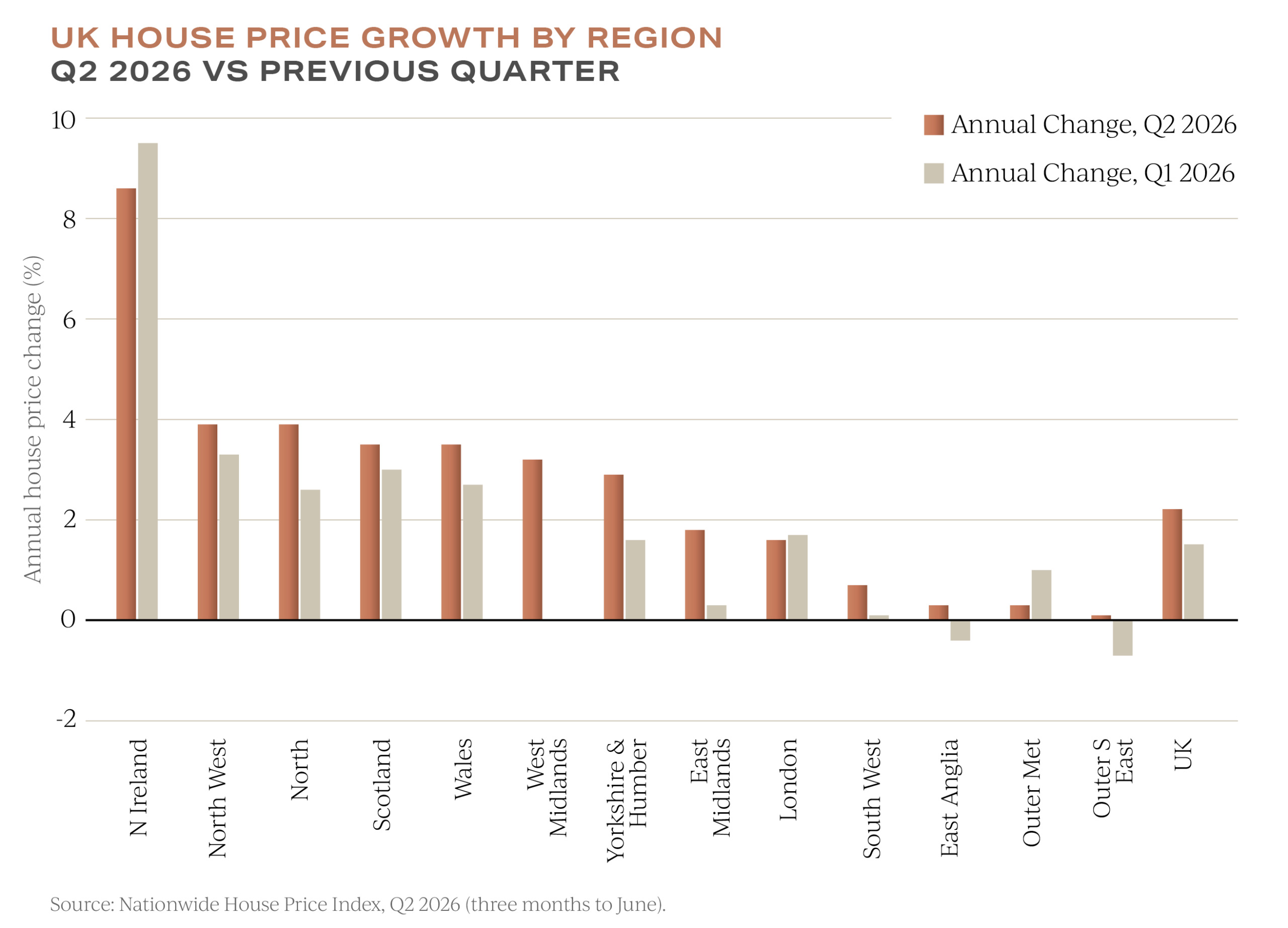

The clearest divide remains regional house prices. Nationwide records that Northern Ireland’s average house price is up 8.6%, and in the North West prices are up 3.9% over the year, while growth across southern England has all but stalled.

The divide runs through property types too, with well-priced houses selling at close to last year’s pace while flats and overpriced stock wait far longer.

Garrington sees this less as a weak market than a divided one, sorting itself by affordability, quality and readiness. For sellers the lesson is that pricing must reflect today’s buyer pool, not last year’s comparable.

As July unfolds, the UK property market looks finely balanced rather than falling. Mortgage rates have eased from their spring peak, and sellers are trimming asking prices to meet buyers rather than holding out for prices that belong to an earlier market.

Well-priced family homes in sought-after locations still attract genuine interest, while overpriced stock and homes just above a key tax threshold face a more demanding audience. For anyone weighing a move, conditions favour the buyer: more choice, generally less competition, and more realistic sellers, an advantage that may not outlast the return of political clarity.

If the summer pause gives you space to think about a move, or you would like to know how these shifts affect a specific location or price bracket, the Garrington team would be glad to help. Please get in touch.

Welcome to Garrington’s June UK property market review, where another month of competing data and conflicting headlines is...

Welcome to Garrington’s latest UK property market review. May is the first month this year in which both the...

Welcome to Garrington’s latest UK Property Market Review. The clocks have sprung forward, the evenings are lengthening, and...