UK Property Market July 2026: Repricing, Not Retreating

Welcome to Garrington’s July UK Property Market Review. Summer is now in full swing, bringing Wimbledon, the cricket, a...

Welcome to Garrington’s June UK property market review, where another month of competing data and conflicting headlines is making buyers and sellers question where the market is heading.

In truth, there is no single answer. It depends on area, property type, price sector, and buyer demographic, and what is true above £2 million bears little resemblance to what is true under £500,000.

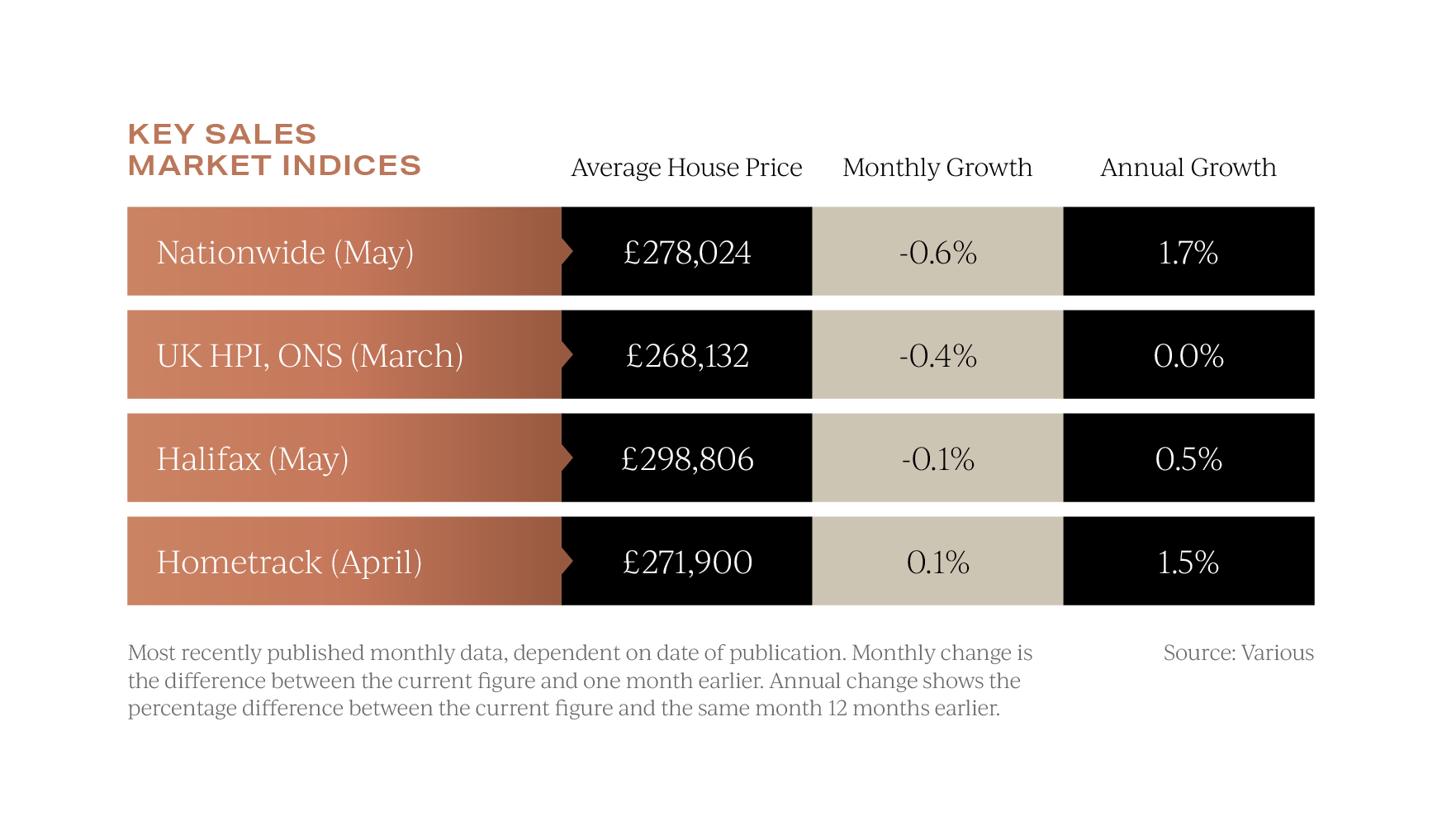

At a headline level, the market is resilient but restrained. Nationwide shows annual price growth slowing to 1.7% in May, while Halifax reports prices fell by 0.1% last month. Zoopla puts average UK house price inflation at 1.5%, with sales agreed marginally ahead of last year despite buyer demand being around 10% lower. Garrington reads this as a market in which committed buyers are still acting, cautious buyers are stepping back, and sellers must therefore close the gap between their aspirations and what the market will tolerate.

Zoopla puts average UK house price inflation at 1.5%, with sales agreed marginally ahead of last year despite buyer demand being around 10% lower. Garrington reads this as a market in which committed buyers are still acting, cautious buyers are stepping back, and sellers must therefore close the gap between their aspirations and what the market will tolerate.

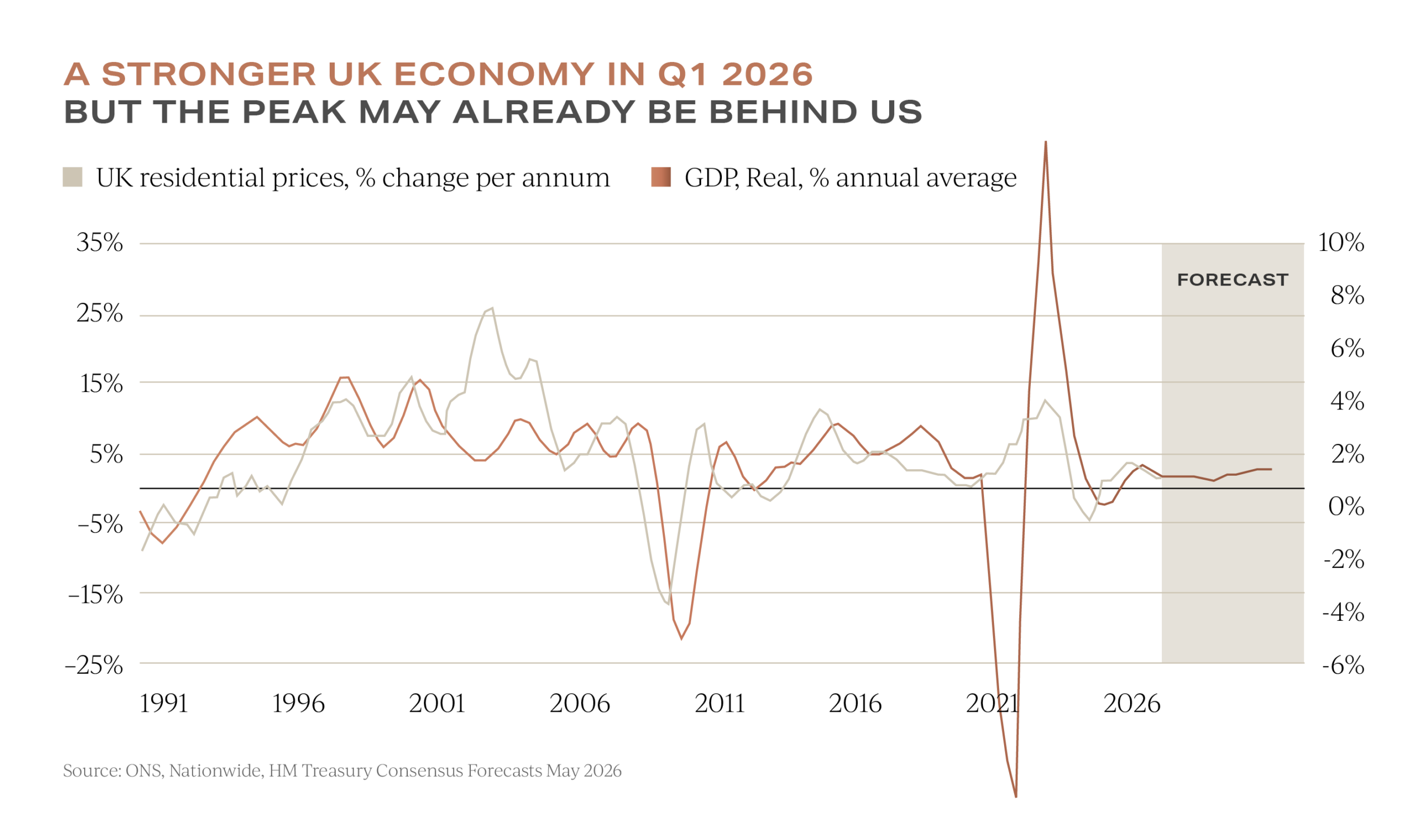

The economy entered this stretch of uncertainty in better shape than expected. UK GDP grew by 0.6% in Q1, a marked step up from the 0.1% to 0.2% figures we had become accustomed to. The full economic effect of the Middle East conflict had not yet fed through, so the headline data reads slightly rosier than the underlying mood.

The more useful signal, in Garrington’s view, is the direction of forecasts. Consensus expectations for 2026 growth have been quietly upgraded from around 0.6% to closer to 1.0%, with Q1 probably the year’s high-water mark.

The implication for housing is low single-digit national growth, with variations locally, and affordability remains the gatekeeper. The genuine upside swing factor is productivity, particularly any pull-through from AI, though the timing is impossible to predict.

The implication for housing is low single-digit national growth, with variations locally, and affordability remains the gatekeeper. The genuine upside swing factor is productivity, particularly any pull-through from AI, though the timing is impossible to predict.

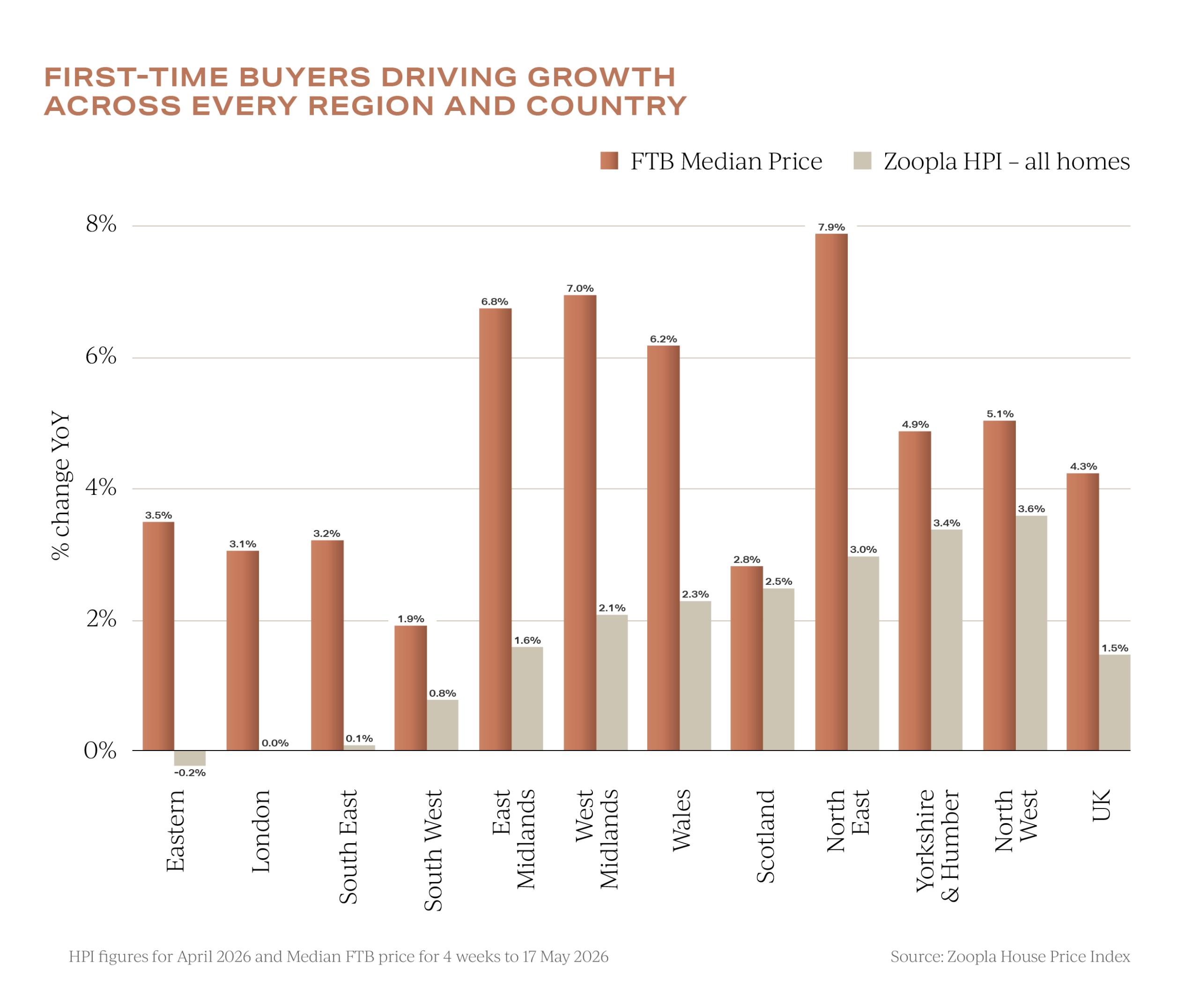

The mainstream end of the market remains the most active, with well-priced homes moving regardless of geography. Hometrack shows fewer first-time buyers this year, but those still pursuing a purchase are not compromising and are searching for homes priced around £10,000 higher than a year ago.

Affordability, by our reading, is concentrating demand at the entry level rather than destroying it, and driving growth in this price sector. Rightmove tells the same story regionally, with prices rising in the North East and North West while London and the South East are softer, and with buyer choice at its highest for this time of year in more than a decade, around a third of listings have already seen a price reduction.

Rightmove tells the same story regionally, with prices rising in the North East and North West while London and the South East are softer, and with buyer choice at its highest for this time of year in more than a decade, around a third of listings have already seen a price reduction.

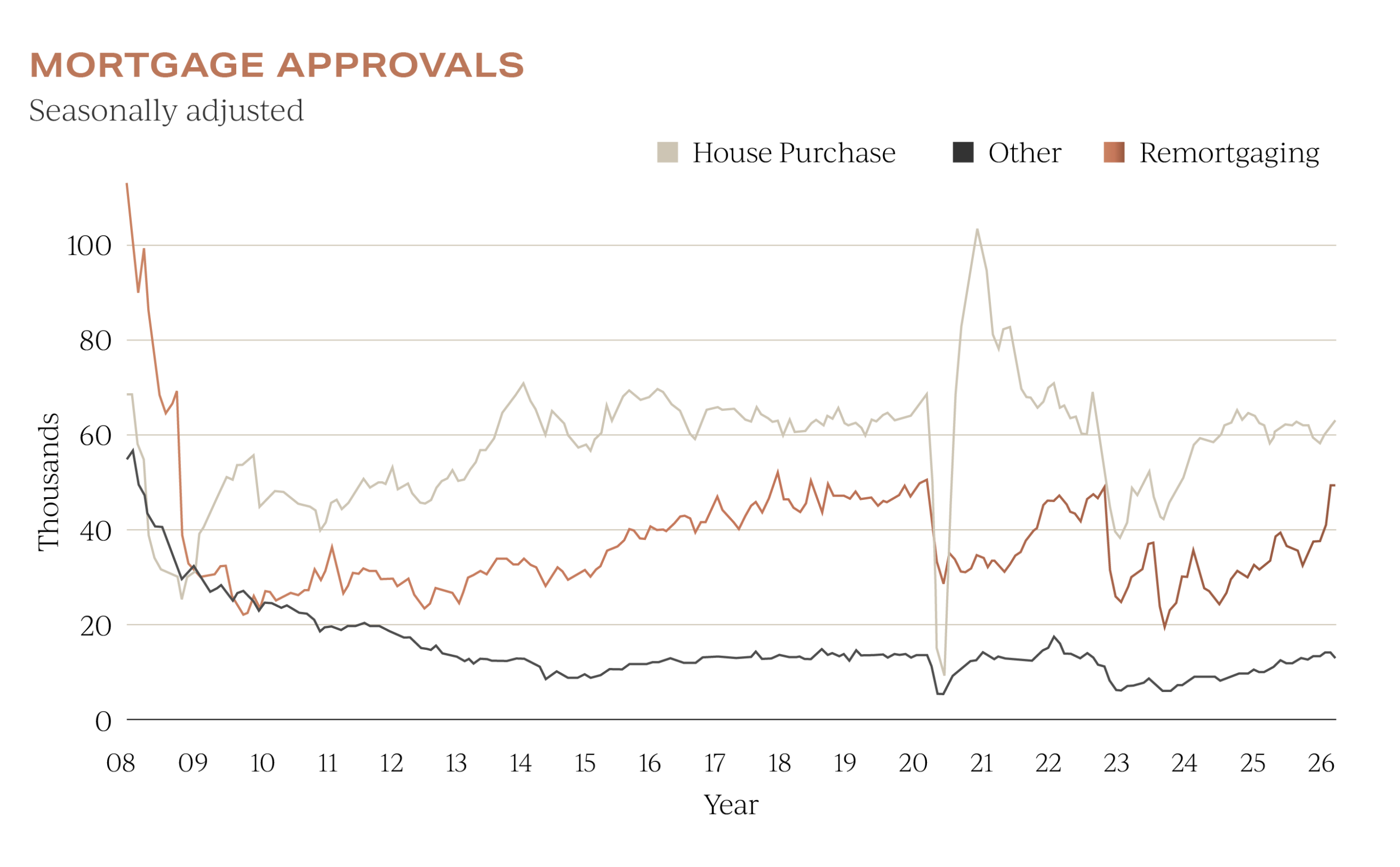

The Bank of England’s data reinforces the picture: mortgage approvals rose to 65,900 in April, comfortably above the six-month average, even as net borrowing eased sharply to £4.4 billion from £6.8 billion in March. The data points to a market that is still functioning, but one in which financial discipline is clearly shaping activity.

At the upper end of the UK property market, Garrington’s view diverges from the headlines. Above £2 million, outside of London, conditions are inherently slower, with an oversupply of stock and a narrower pool of proceedable buyers, while between £1 million and £2 million, activity moves forward only where pricing feels fair and defensible.

This is a stand-off rather than a slump. Much of the stock above £2 million is held by older homeowners who would like to right-size but are not financially compelled to move, with many unencumbered by debt. They want the maximum exit value on their existing home, which in today’s buyer pool is often not available, so they are choosing patience over compromise.

There is lifestyle motivation in the upper market but no distress, and that combination means best-in-class homes still attract real interest while compromised stock drifts into extended marketing and reductions.

London is traditionally viewed as the barometer for the wider UK property market, even though it is intrinsically decoupled by value, wealth concentration, and international influence. It tends to lead alone, and when it lags, it lags alone.

The question Garrington hears from clients has shifted. It is no longer “should I avoid London?” but “is London starting to look good value again?”, and our view is yes, selectively and postcode by postcode.

Oversupply still weighs heavy on pricing, but the pool of value-based buyers has grown notably this year, and for those able to take a longer-term view, the window has the feel of an opportunity.

Hometrack has London sales agreed running 8% ahead of last year, the strongest regionally, while LonRes describes prime London as showing tentative signs of improvement, with the average discount from initial asking price at a seven-year high. And as ever, sought-after properties with prime addresses attract interest and are selling.

For all the noise, the underlying picture is straightforward. The mainstream market is moving because disciplined buyers are meeting realistically priced stock; the upper market is in stand-off, waiting for pricing realism from sellers or a return of buyer confidence; and London is offering pockets of genuine value to those prepared to look closely.

The market is sorting itself by quality, price discipline, and buyer intent, and for sellers, the lesson is unavoidable: pricing accurately on day one is essential, because optimism in the asking figure is usually paid back in time on the market and reductions later.

If you are forming your own property plans this summer, or want to understand how these conditions apply to a specific location or price bracket, Garrington would be pleased to help. Please get in touch.

Welcome to Garrington’s July UK Property Market Review. Summer is now in full swing, bringing Wimbledon, the cricket, a...

Welcome to Garrington’s latest UK property market review. May is the first month this year in which both the...

Welcome to Garrington’s latest UK Property Market Review. The clocks have sprung forward, the evenings are lengthening, and...