UK Property Market July 2026: Repricing, Not Retreating

Welcome to Garrington’s July UK Property Market Review. Summer is now in full swing, bringing Wimbledon, the cricket, a...

A warm welcome to Garrington’s latest UK property market review.

After a spring defined by volatility and economic headwinds, June arrived with a sense of recalibration in the UK housing market. The balmy weather and long Bank Holiday weekends have seemingly nudged both buyers and sellers into action, and the early summer mood feels notably more purposeful than it did just a month ago.

While April delivered a hard reset for many regions as activity fell back following the stamp duty deadline, May marked a cautiously optimistic return to form. Buyer demand has reawakened, underpinned by falling mortgage rates and signs that the worst of the challenging economic conditions may now be behind us.

Garrington is seeing renewed confidence among domestic buyers, many of whom had adopted a ‘wait-and-see’ approach earlier in the year but are now actively embarking on their searches.

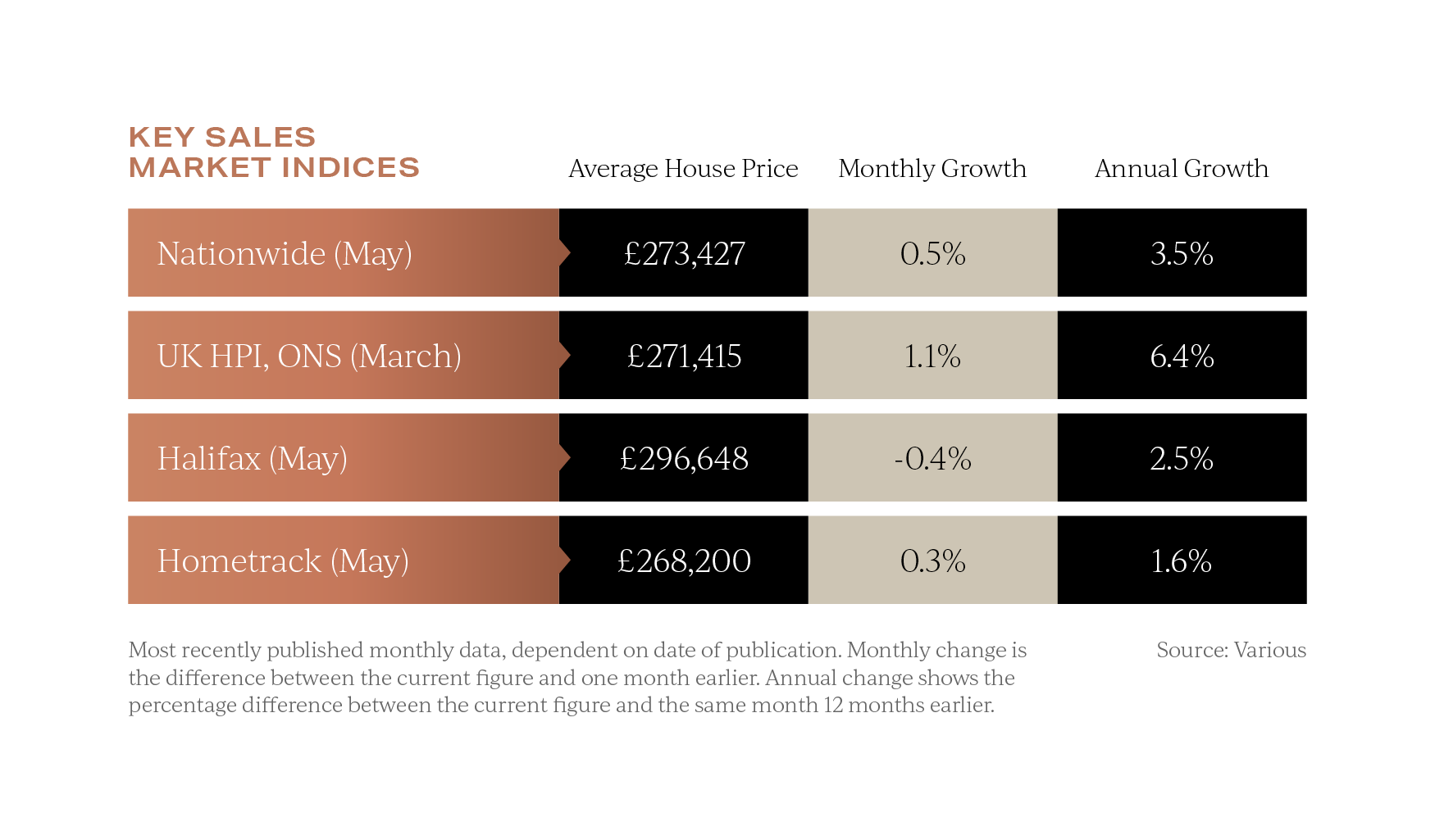

House prices continued to edge higher in May. In terms of new stock entering the UK property market, Rightmove’s latest data shows that average asking prices reached a record high of £379,517, but this was the smallest May increase since 2016, reflecting the weight of growing supply.

Nationwide reported a 0.5% monthly rise in average house prices, reversing April’s dip and lifting annual growth to 3.5%, the strongest reading since late 2023. This is in complete contrast to Halifax’s latest data, which records a -0.4% fall in average house price values.

This is in complete contrast to Halifax’s latest data, which records a -0.4% fall in average house price values.

However, national averages obscure a deepening regional divide. Garrington’s observations suggest a price recalibration is underway in much of southern England where increased stock is meeting more selective demand.

In contrast, prices in many parts of northern England and Scotland continue to rise at pace, driven by relative affordability and resilient local demand. Prices in the North West and Scotland are 3% higher year-on-year, with areas such as Blackburn and Belfast recording gains above 5% according to HomeTrack.

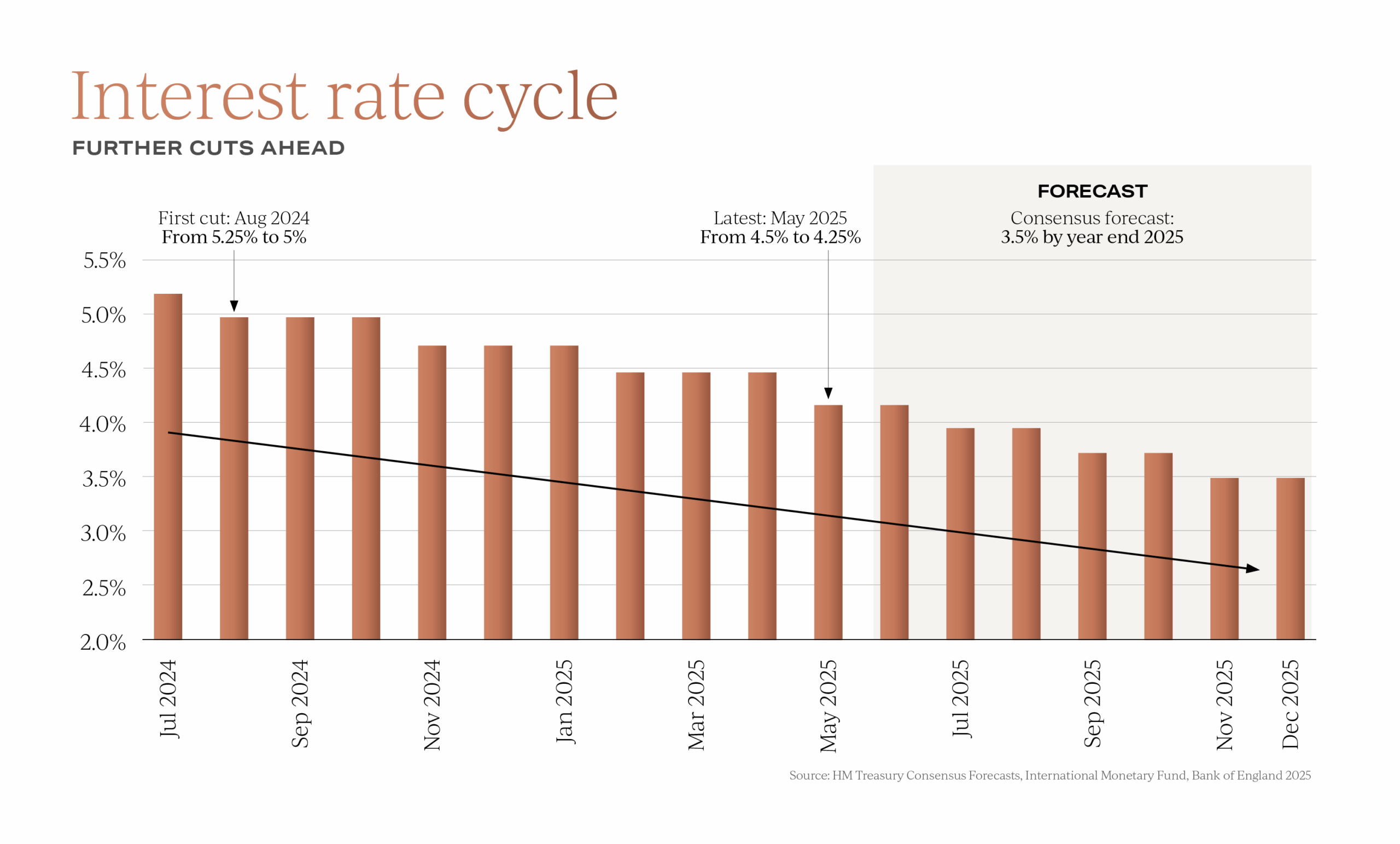

Last month’s base rate cut by the Bank of England from 4.5% to 4.25% was modest but symbolic; it marked the second reduction in the current cycle and reinforced consensus expectations for further cuts by year-end. The Treasury forecast now points to a base rate of 3.5% by December. Mortgage lenders were quick to react. Garrington has observed a flurry of repricing activity, with several high street lenders reducing rates below 4% for the first time in over a year. This easing is helping to rebalance affordability, particularly in high-value areas, such as London and the South East.

Mortgage lenders were quick to react. Garrington has observed a flurry of repricing activity, with several high street lenders reducing rates below 4% for the first time in over a year. This easing is helping to rebalance affordability, particularly in high-value areas, such as London and the South East.

There is also growing evidence that buy-to-let borrowers are re-entering the UK property market, encouraged by improved yields and lower borrowing costs.

Garrington is seeing renewed interest from private investors exploring income-led acquisition strategies, as savings rates and returns from other investment asset classes falter.

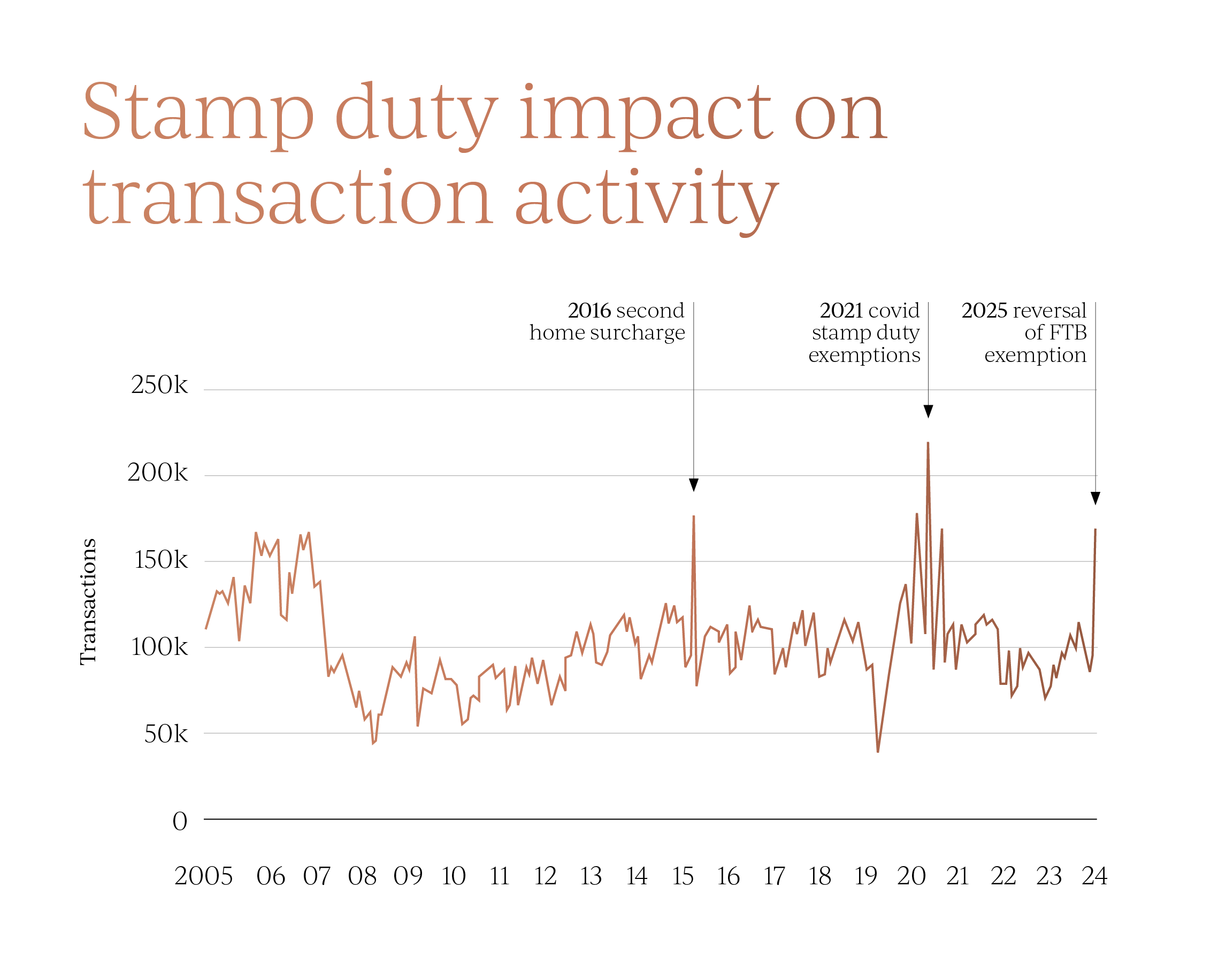

The spring surge in transactions in the mainstream market, largely driven by first-time buyers racing to beat the stamp duty change; left a lasting imprint on the latest transaction volume data.

HMRC recorded 164,650 residential transactions in March alone, equating to a 69% increase on the 20-year average. Although some of this demand has clearly been brought forward, early indicators for the rest of the year remain reasonably robust. The number of sales agreed is now 5% higher than this time last year based on Rightmove’s latest data. Likewise, Zoopla reports that the volume of sales agreed in May was the highest in four years, while supply is also up 13% year-on-year.

The number of sales agreed is now 5% higher than this time last year based on Rightmove’s latest data. Likewise, Zoopla reports that the volume of sales agreed in May was the highest in four years, while supply is also up 13% year-on-year.

Garrington is seeing a notable volume of formerly withdrawn properties being re-launched, often at revised prices, as vendors realign their expectations to the realities of the current market.

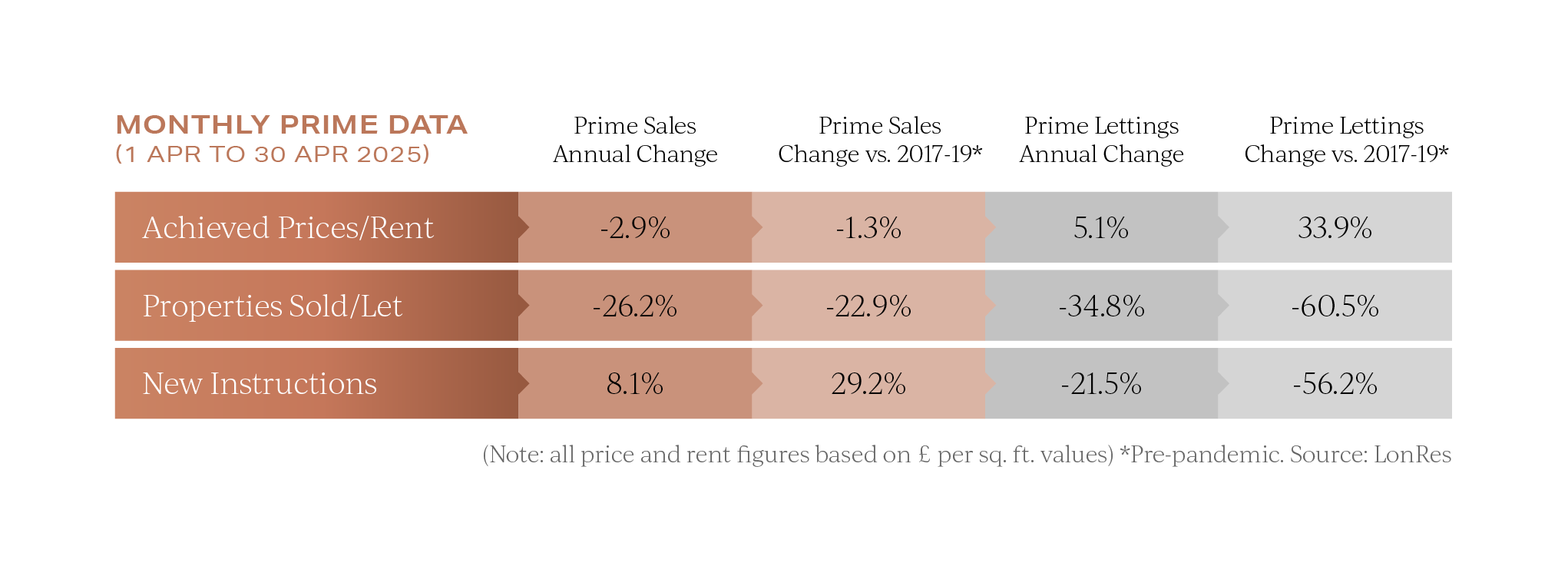

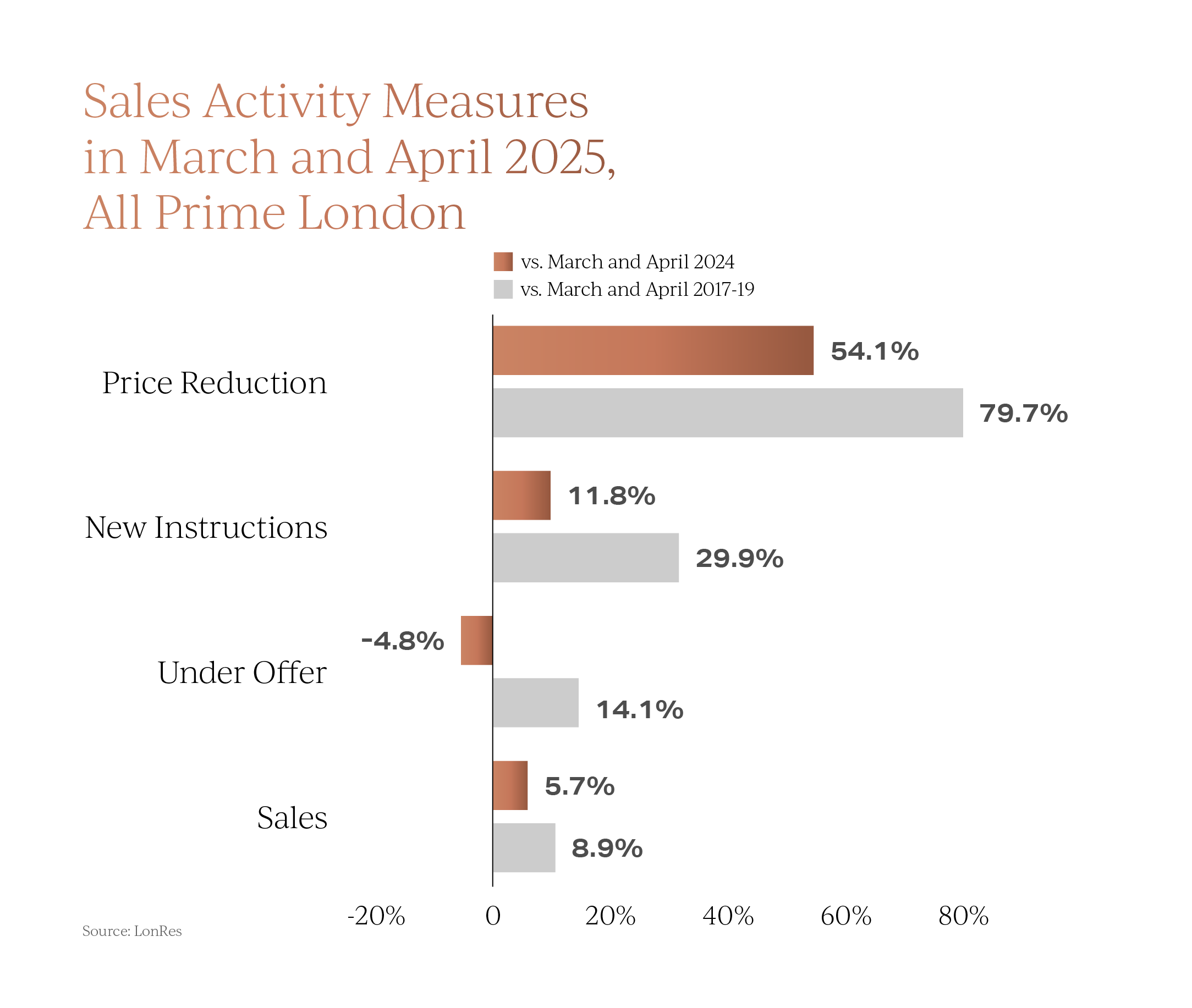

In Prime Central London and other high-value markets, a quieter tone persists. The average price achieved in the capital fell by 2.9% year-on-year in April, with discounts to original asking prices averaging 8.9%. However, the volume of new instructions continues to climb, with those in London up by 11.8%.

However, the volume of new instructions continues to climb, with those in London up by 11.8%. Garrington has, on many occasions, successfully negotiated significant price reductions for clients in these locations, where buyer sentiment remains cautious yet engaged. Pricing realism is key.

Garrington has, on many occasions, successfully negotiated significant price reductions for clients in these locations, where buyer sentiment remains cautious yet engaged. Pricing realism is key.

With the exception of American buyers, the pattern Garrington is seeing in the Prime London market is that buyers are often domestic, longer-term movers rather than speculative investors, and they are increasingly willing to walk away from overpriced stock.

While the extraordinary activity seen in March may not be repeated, the UK property market appears to have avoided a post-stamp duty deadline slump.

With interest rates falling, buyer confidence improving, and price growth returning to sustainable levels, conditions remain supportive for those seeking to transact this summer.

The prevailing theme is one of recalibration rather than resurgence. Buyers remain discerning, and value-led strategies are being rewarded.

For those at the early stages of planning a move, Garrington’s Best Places to Live research provides a valuable resource. The interactive tool allows users to compare locations across the UK based on a range of lifestyle and investment factors, helping buyers shape their thinking and refine their search.

Garrington’s team of advisors are here to help you navigate the market and secure the right property with confidence. To discuss your plans, please do get in touch.

Welcome to Garrington’s July UK Property Market Review. Summer is now in full swing, bringing Wimbledon, the cricket, a...

Welcome to Garrington’s June UK property market review, where another month of competing data and conflicting headlines is...

Welcome to Garrington’s latest UK property market review. May is the first month this year in which both the...