UK Property Market July 2026: Repricing, Not Retreating

Welcome to Garrington’s July UK Property Market Review. Summer is now in full swing, bringing Wimbledon, the cricket, a...

Welcome to the May edition of Garrington’s review of the UK property market.

As the UK enjoyed a rare run of bank holidays under bright blue skies, the UK property market has entered a more complex phase. April’s data confirms that the market remains resilient, but not without friction.

Despite seasonal optimism, renewed global headwinds and the phased withdrawal of stamp duty relief have introduced a more cautious undercurrent.

New records for asking prices and above-average transaction volumes suggest buyers are still active, albeit more discerning. With some leading indicators softening and buyer sentiment more finely balanced, could this be a seasonal peak, or simply a pause before the next gear change?

Headline house price data showed mixed results in April. Halifax recorded a 0.3% monthly rise in average prices and a 3.2% annual gain, with the average property now priced at £297,781.

Nationwide, in contrast, reported a fall in average prices of 0.6% for the month and a 3.4% annual growth rate. Meanwhile, Rightmove saw a strong seasonal uptick, with asking prices rising 1.4% to a record £377,182, underpinned by a 5% annual increase in buyer demand.

Meanwhile, Rightmove saw a strong seasonal uptick, with asking prices rising 1.4% to a record £377,182, underpinned by a 5% annual increase in buyer demand.

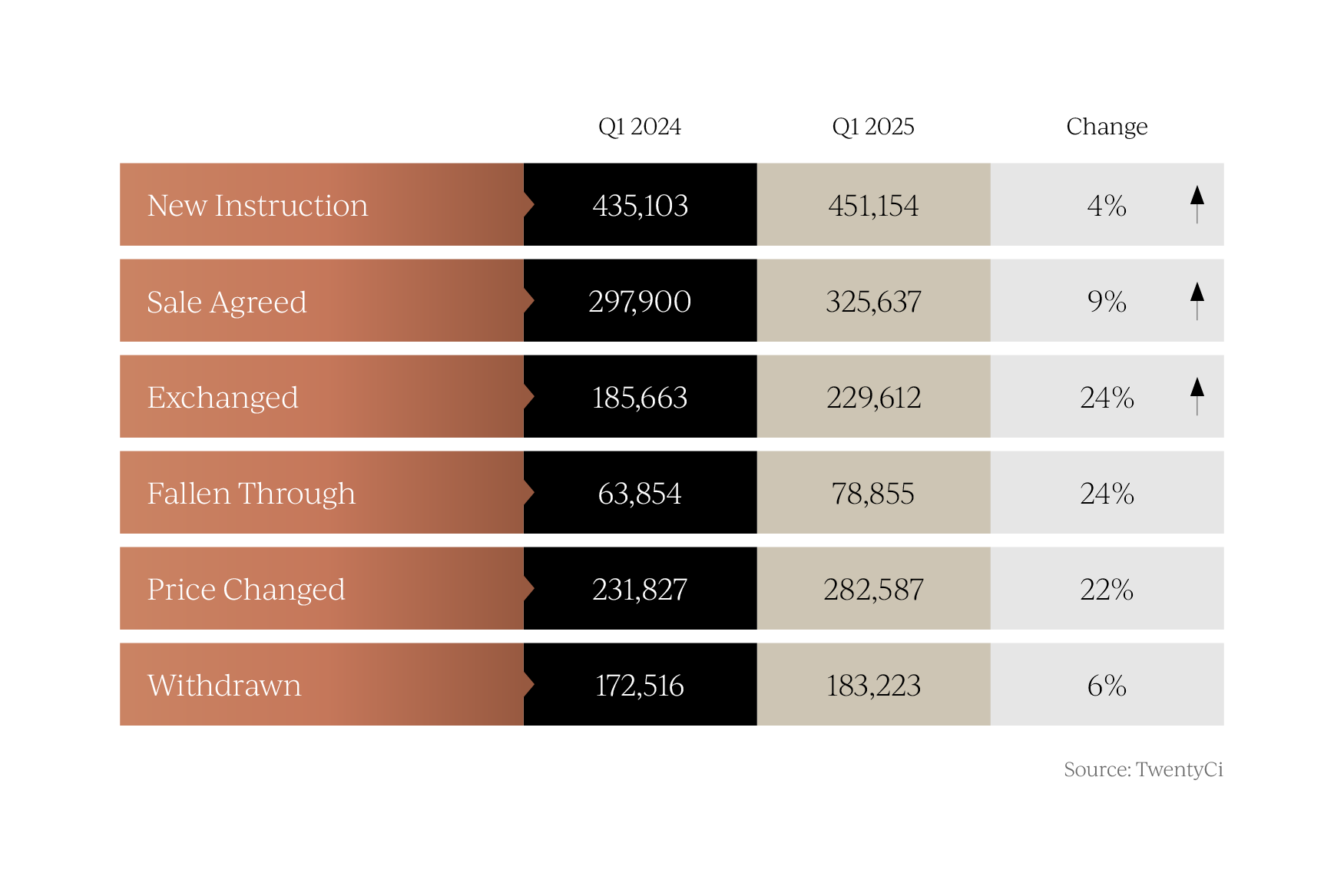

Despite these latest indicators, annual price growth appears to be flattening. Zoopla’s index, based on completed sales, shows a 1.6% annual rise, up from 0.2% a year ago, but trending down since December. The key driver of stability remains supply, with TwentyCi data confirming 451,000 new listings in Q1, the highest seen in seven years.

The key driver of stability remains supply, with TwentyCi data confirming 451,000 new listings in Q1, the highest seen in seven years. Garrington is observing a more polarised market. Realistic pricing continues to unlock sales, but over-ambitious vendors are increasingly having to reduce prices this spring. Regional disparities are also becoming more pronounced.

Garrington is observing a more polarised market. Realistic pricing continues to unlock sales, but over-ambitious vendors are increasingly having to reduce prices this spring. Regional disparities are also becoming more pronounced.

At the lower end of the market, the rush to complete ahead of April’s stamp duty changes created a short-term surge in completions. HMRC’s data shows March volumes were up 62% month-on-month and more than double compared to a year ago.

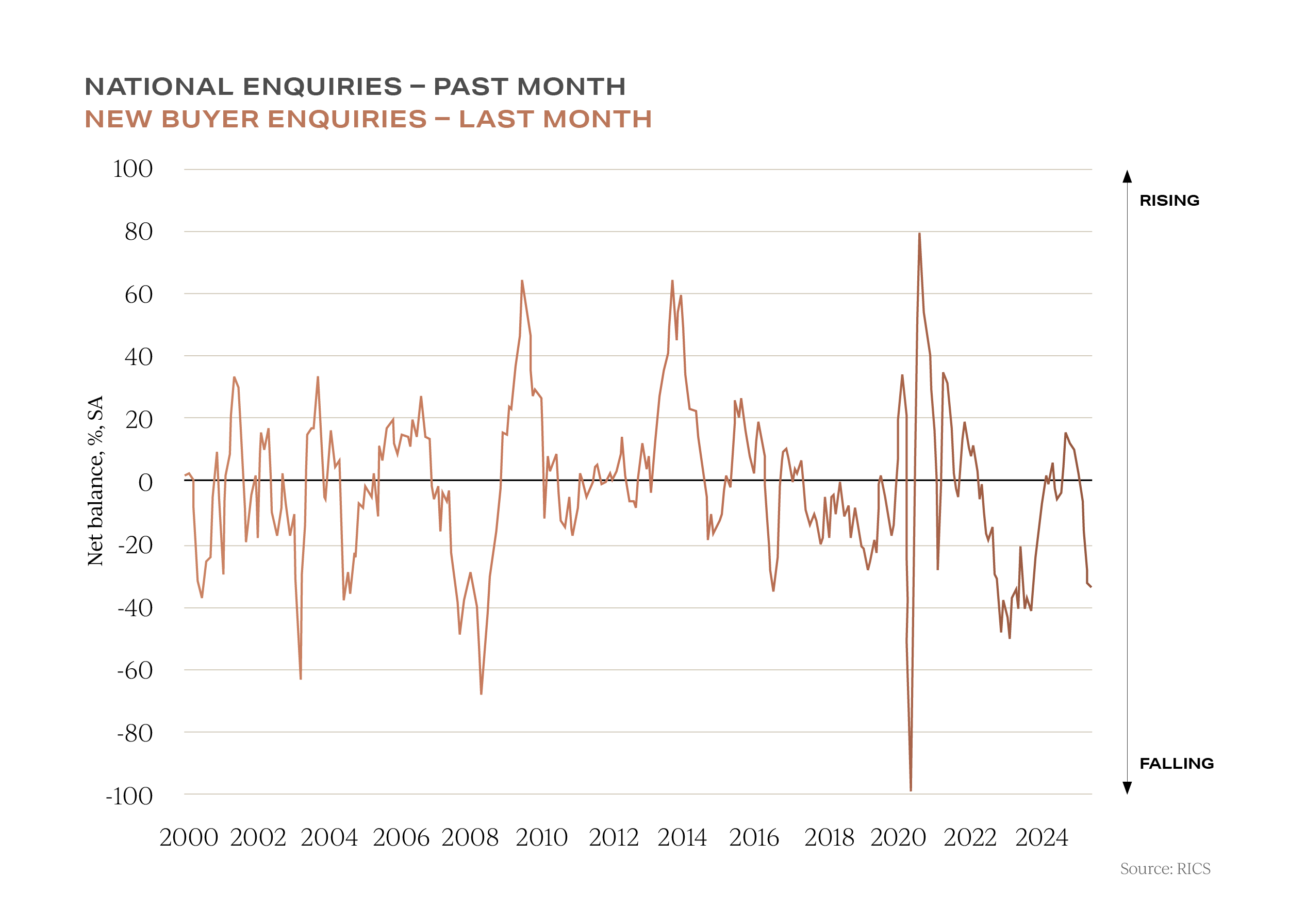

Momentum is unlikely to persist, however RICS reports a net balance of -33% for new buyer enquiries in April and -31% for sales agreed, the weakest since August 2023. That said, a net +17% of agents still expect transactions to rise over the next year.

Garrington is seeing a steady flow of committed buyers, though some are now pausing plans amid economic and political uncertainty.

Until last week, global trade tensions notably between the UK-US were a concern and a drag on the market. However, the welcome confirmation of a full UK-US trade deal could materially boost confidence over the coming months, subject to clarification on the details of the agreement.

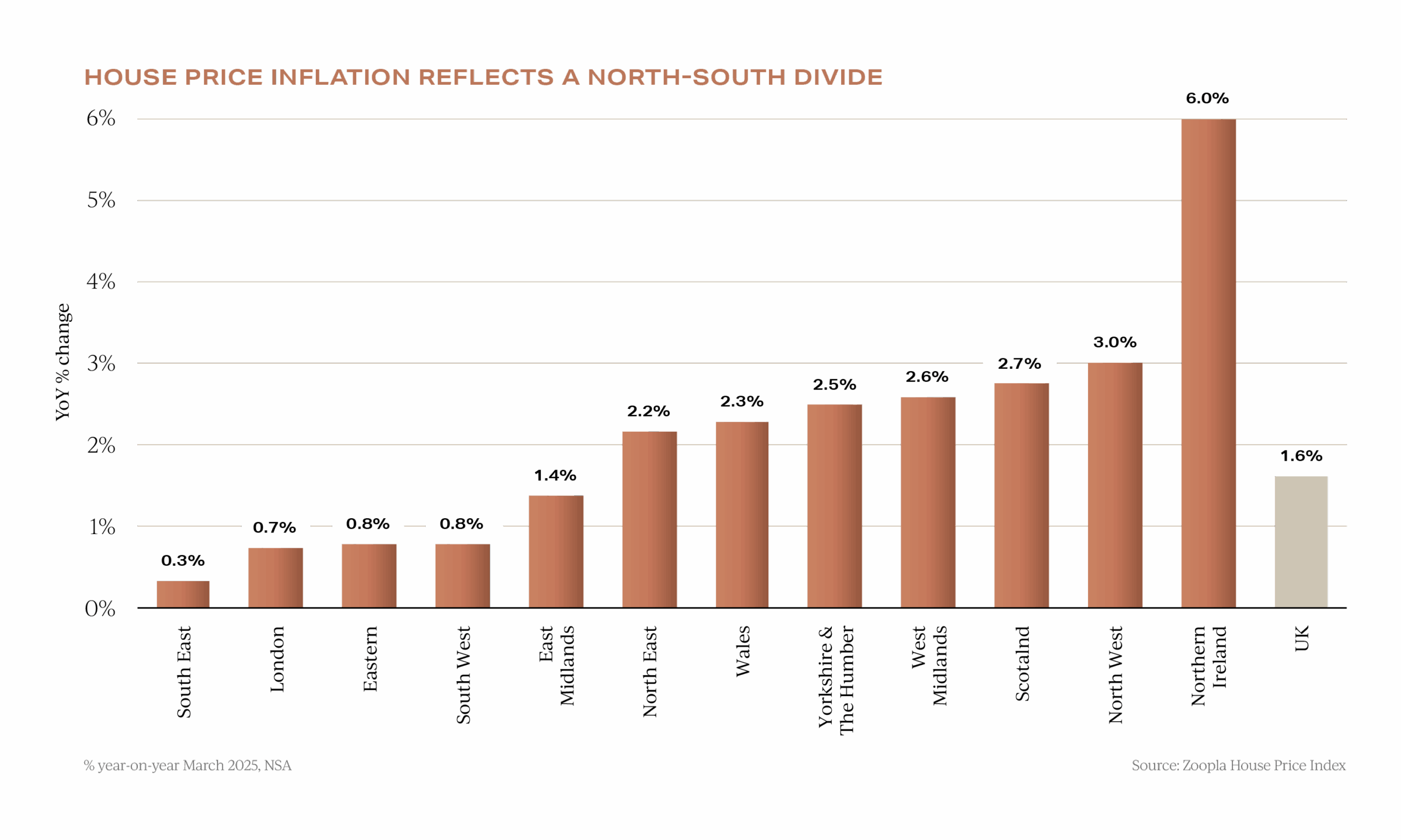

April brought a further reversal in the north-south divide of average house prices. Halifax data shows Northern Ireland leading with +8.1% annual growth, followed by Wales and Scotland. The North West was England’s best performer at +4.1%, while London and the South West trailed.

Rightmove also reports new asking price records across all Midlands and Northern regions. Garrington is seeing rising interest in cities offering better value, including Manchester and Newcastle.

By contrast, southern markets are facing oversupply and slower sales.

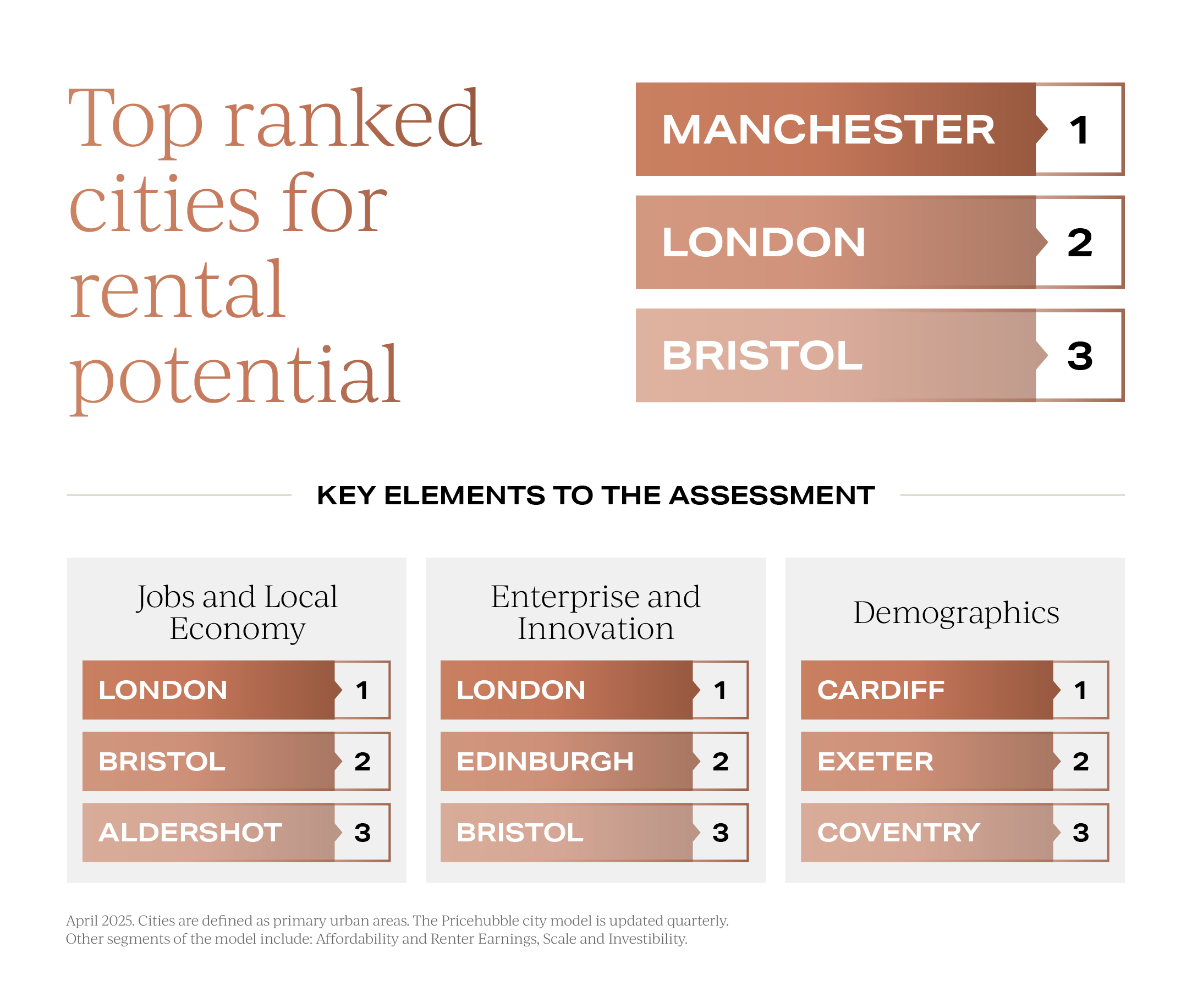

The South East is now the hardest region in which to secure a sale, with a 26.5% fall-through rate and only half of listings converting into successful sales, based on latest data from TwentyCi. Longer term investment potential for London and southern cities remains strong however. Whilst Manchester ranked first place, London and Bristol are the next top-ranking places for rental potential according to the latest City Ranking Model from PriceHubble.

Longer term investment potential for London and southern cities remains strong however. Whilst Manchester ranked first place, London and Bristol are the next top-ranking places for rental potential according to the latest City Ranking Model from PriceHubble.

The ranking model draws on economic, demographic and housing market data to assess the outlook for rental demand across the UK’s largest 60 towns and cities.

Easing financial conditions are reshaping buyer behaviour. Mortgage rates are now widely closer to 4% for high-LTV borrowers, with sub-4% two and five-year deals returning for those with 25% deposits or more.

In a significant move, the Bank of England has cut the base rate to 4.25%, its second cut this year. Combined with moderating inflation, this is improving affordability.

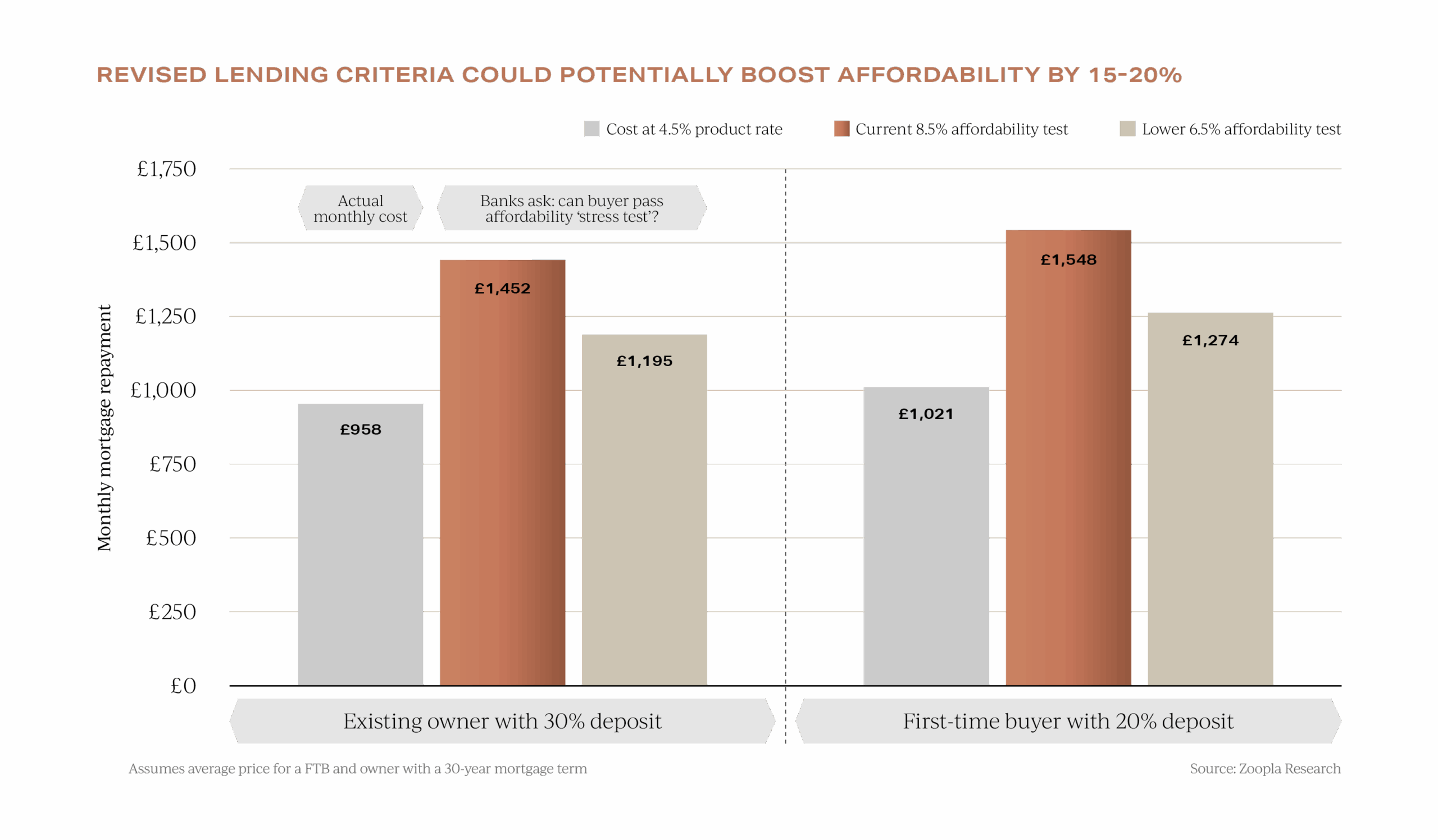

Although the average five-year fixed mortgage rate currently sits at around 4%-4.5%, many lenders are still stress-testing applicants’ affordability at rates between 8% and 9%. This significantly reduces borrowing capacity unless a substantial deposit is available.

This significantly reduces borrowing capacity unless a substantial deposit is available.

If these stress-test rates were to ease back to their pre-2022 range of 6.5% to 7%, it could enhance buyers’ purchasing power by as much as 15% to 20%.

Latest Bank of England data shows mortgage approvals are up 4.5% year-on-year.

Garrington is already seeing that better finance options are reigniting interest from buyers, whether upsizing or downsizing, looking to restructure borrowing or commence previously postponed moving plans.

As spring shortly gives way to summer, the UK property market remains active but more complex. While macro data signals resilience, evolving regional dynamics and affordability are shaping new realities.

With borrowing costs now falling and the prospect of a new UK-US trade deal lifting both investor sentiment and consumer confidence, conditions are improving. For buyers and sellers alike, understanding local trends and acting decisively will be key.

For those at the early stages of planning a move, Garrington’s newly released Best Places to Live research provides a valuable resource. The interactive tool allows users to compare locations across the UK based on a range of lifestyle and investment factors, helping buyers shape their thinking and refine their search.

Garrington’s team of advisors are here to help you navigate the market and secure the right property with confidence. To discuss your plans, please do get in touch.

Welcome to Garrington’s July UK Property Market Review. Summer is now in full swing, bringing Wimbledon, the cricket, a...

Welcome to Garrington’s June UK property market review, where another month of competing data and conflicting headlines is...

Welcome to Garrington’s latest UK property market review. May is the first month this year in which both the...